An Economic Assessment of the 765-kV Strategic Transmission Expansion Plan

And Alternative Approaches to Enable Cost-Effective Growth

WRITTEN BY Brent Bennett, Ph.D.

Download the full research paper here.

KEY POINTS

• The need for the 765-kV STEP is driven by an overbuilding of wind and solar across Texas, particularly in West Texas and South Texas, and the plan does not address the need to increase the supply of reliable generation.

• Considerable private investment in reliable generation will be needed with or without new transmission. The 765-kV lines alone will reduce spending on new generation and transmission by no more than 2% through 2038.

• The 765-kV lines will not measurably impact energy prices in ERCOT. Eliminating the lines and building new gas generation near demand will yield almost identical future price outcomes.

• Adding 4-5 GW of gas generation in West Texas and shifting some generation across the other regions of the ERCOT grid could eliminate the need for the 765-kV lines.

EXECUTIVE SUMMARY

This paper argues that Texas policymakers should pause implementation of ERCOT’s 765-kV Strategic Transmission Expansion Plan (STEP) and consider alternatives to minimize the cost and impact of the future transmission buildout. The STEP—which includes the Permian Basin Reliability Plan and related long-distance transmission projects approved through December 2025—would impose nearly $100 billion in lifetime costs on Texas ratepayers and result in irreversible property losses for thousands of landowners across the state. Unlike the Competitive Renewable Energy Zones, which were specifically created by the Texas Legislature in 2005 (SB 20, 2005), the STEP was approved without legislation.

The 765-kV STEP is built on many assumptions that are fundamentally driven to satisfy the desire of large industrial consumers—from oil and gas majors to new data centers—to purchase more wind and solar from across Texas to leverage wind, solar, and battery tax credits and/or to chase their corporate emissions goals. The study from Energy Ventures Analysis contained here finds that the 765-kV lines do not materially change ERCOT’s long-term generation mix and leave future price outcomes largely unchanged when compared with scenarios that rely more heavily on properly located gas generation. The 765-kV lines are not needed to meet demand from Texas households and small businesses. Their primary rationale is to help ERCOT manage a future system with ever more wind and solar power connecting to the grid to meet growing industrial demand.

In other words, the projects in the 765-kV STEP, particularly the 765-kV lines themselves, are a policy choice, not an economic or reliability necessity. ERCOT and the PUC did not examine whether cheaper, more reliable alternatives—especially properly sited dispatchable generation closer to demand—could achieve the same or better reliability outcomes with fewer land-use impacts and lower costs to ratepayers. A generation-first framework that prioritizes reliable capacity near load centers, stronger market incentives for dispatchable generation, and targeted tools to manage large new loads, such as data centers, would better align with the goals of the Legislature (HB 5066, 2023a) and achieve better outcomes for all Texans. In addition to reevaluating the STEP, the Legislature should require a more transparent public planning process for statewide transmission projects and ensure that ERCOT’s planning protects consumers and property owners rather than shifting risk and cost onto the public for the benefit of a narrow set of stakeholders.

INTRODUCTION TO THE 765-KV STRATEGIC TRANSMISSION EXPANSION PLAN (STEP)

The purpose of this study is to assess the economic and reliability impacts of the 765-kV Strategic Transmission Expansion Plan (STEP), which was developed by the Public Utility Commission of Texas (PUC) and the Electric Reliability Council of Texas (ERCOT) in response to legislation that required the development of reliability plans for regions with rapid electric demand growth, specifically the Permian Basin (HB 5066, 2023a). The Texas Public Policy Foundation partnered with Energy Ventures Analysis to perform techno-economic modeling of the 765-kV STEP, a detailed summary of which is attached to the end of this paper. The material below summarizes the modeling results, explains the history of the 765-kV STEP, and assesses alternative policy solutions for building the new transmission.

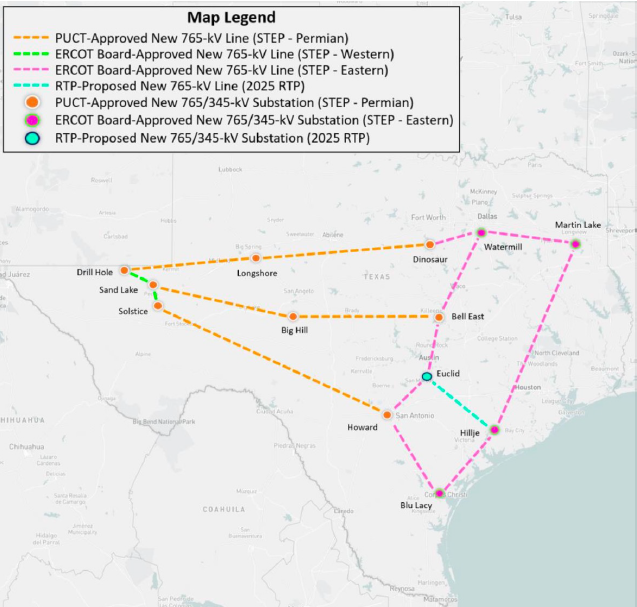

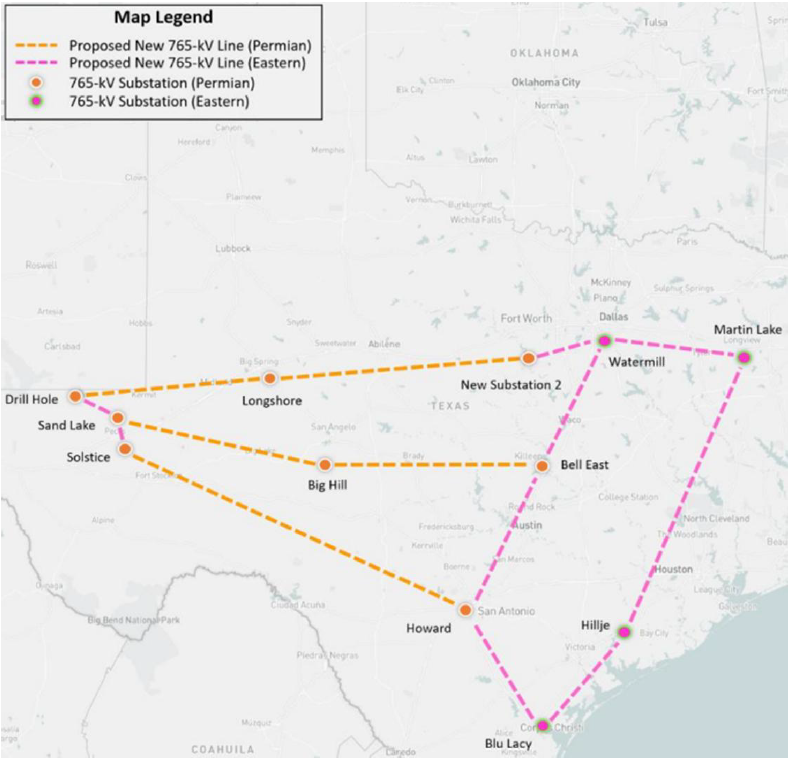

The map in Figure 1 shows the extent of the 765-kV projects approved to date. In addition to the $17.2 billion estimated cost of the 765-kV lines, ERCOT and the PUC have approved $4.7 billion in local transmission upgrades in the Permian and $11 billion in upgrades that accompany the 765-kV lines in other regions (ERCOT, 2025a, p. 8). If the $33 billion capital cost estimate holds, the lifetime cost of these projects—including financing, equity returns, maintenance, and taxes—will be nearly $100 billion (Bennett & Priacci, 2026, p. 10).

This study covers only projects that have been approved by December 2025, which are the pink, orange, and green lines in Figure 1 (not the teal line). The orange projects are covered by the Permian Basin Reliability Plan (PBRP), approved by the PUC in April 2025, and the pink and green projects are the remaining 765-kV STEP approved by the ERCOT board in December 2025. The study will project the type and quantity of new generation built and the total energy costs to ratepayers in three different scenarios: (1) the base case with no 765-kV lines, (2) the PBRP lines only, and (3) the entire 765-kV STEP. Before we explain those results, it is important to understand the history of the PBRP and the 765-kV STEP, and how the projects these plans propose differ from other transmission projects in ERCOT.

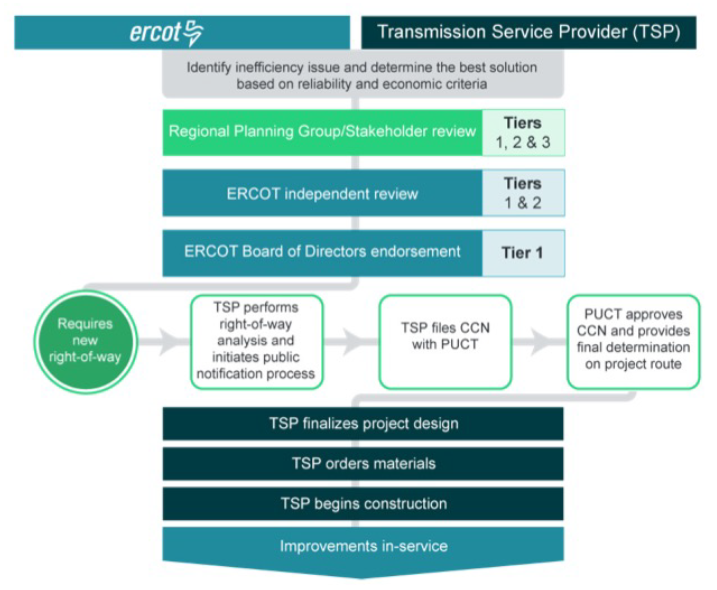

The Transmission Planning Process in ERCOT

Because the ERCOT region has competitive retail and wholesale markets, the PUC cannot dictate the location or type of generation to match demand, as is done in markets with vertically integrated utilities through integrated resource planning. Transmission is the only part of the ERCOT grid that is centrally planned, beginning with ERCOT’s own internal assessments, followed by a stakeholder process and, if needed, the approval of the ERCOT board (ERCOT, 2025b). If a new right-of-way is required, the project undergoes a further layer of review at the PUC, which must grant a certificate of convenience and necessity (CCN) before the transmission utility constructing the project can seize land through eminent domain.

The projects ERCOT is currently reviewing are summarized in the annual regional transmission plan (RTP). Transmission service providers (TSPs) select projects from the RTP to take through the approval process. Projects are divided into four tiers that each require varying layers of review (ERCOT, 2025b).

- Tier 4 projects do not require any input from ERCOT and are typically projects that cost less than $25 million and require no new right of way.

- Tier 3 projects are greater than $25 million, less than $100 million, and do not require new right of way. These projects must be approved by the stakeholder-led Regional Planning Group (RPG).

- Tier 2 projects are the same as Tier 3 projects, except that they require a CCN. These projects must undergo both RPG review and an independent review by ERCOT staff before going to the PUC for final approval.

- Tier 1 projects are any projects, regardless of whether they require a CCN, that are at least $100 million. All of the 765-kV projects fall into this tier. These projects must go through the full stakeholder process and be approved by ERCOT’s board.

Figure 1

Approved and Proposed 765-kV Projects in ERCOT as of December 2025

Note: Figure taken from Report on Existing and Potential Electric System Constraints and Needs, Electric Reliability Council of Texas, December 2025, p. 17 (https://www.ercot.com/files/docs/2025/12/23/2025-Report-on-Existing-and-Potential-Electric-System-Constraints-and-Needs.pdf).

Figure 2

The Transmission Planning Process in ERCOT

Note: Figure taken from ERCOT Trending Topics: ERCOT’s Transmission Planning Process, Electric Reliability Council of Texas, December 2025, p. 5 (https://www.ercot.com/files/docs/2025/08/12/ERCOT_Trending_Topic-Transmission-Planning-Process.pdf).

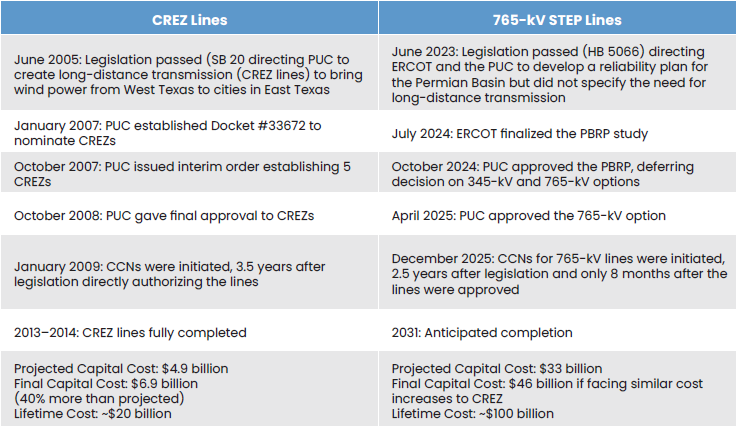

Since the early 2000s, this process has been circumvented on two occasions. The first was the Competitive Renewable Energy Zones (CREZ or CREZ lines), which the Texas Legislature mandated in 2005 (SB20, 2005) to bring wind energy from West Texas to cities in the state’s eastern half. The PUC designated those zones in 2007 (Lasher, 2014, p. 4), initiated the CCNs for the 72 new circuits in 2009, and completed the CCNs by 2011 (p. 7). By the beginning of 2014, the CREZ lines were completed, totaling 3,600 new linear miles of 345-kV lines at a cost of $6.9 billion (p. 8).

The PBRP and the STEP is the second occasion. The Texas Legislature passed HB 5066 in 2023, requiring the PUC and ERCOT to develop a reliability plan for the Permian Basin that would:

- Address extending transmission service to areas where mineral resources have been found;

- Address increasing available capacity to meet forecasted load; and

- Provide available infrastructure to reduce interconnection times in areas without access to transmission service (HB 5066, 2023a, p. 3-4).

Notably, the legislation does not require ERCOT and the PUC to create long-distance import/export lines like the CREZ lines. It also does not preclude the development of generation solutions needed for reliability, which previous legislation directly mandated (SB 3, 2021, pp. 30-31). There was nothing in the legislative record for HB 5066 that indicated the legislation would lead to statewide transmission projects costing tens of billions of dollars. The entire plan came to be under the auspices of the PUC and ERCOT without any votes in the Legislature, despite potentially costing ratepayers four to five times as much as the CREZ.

Table 1

Comparison of Planning and Approval Processes for the CREZ Lines and the 765-kV STEP Lines

Following the passage of the legislation, ERCOT presented its study to the PUC in July 2024 (ERCOT, 2024), and the PUC approved the final plan in October 2024 (PUC, 2024). The PUC delayed a decision on the high-voltage import lines until ERCOT completed a further study of the 345-kV and 765-kV options (ERCOT, 2025a) and then approved the 765-kV option in April 2025 (PUC, 2025). The ERCOT board then approved the remainder of the 765-kV STEP in December 2025 (ERCOT, 2025c). The result was a $33 billion plan, nearly five times the final cost of the CREZ lines, that was never voted on by the Texas Legislature.

Neither ERCOT’s studies nor the PUC’s actions fully satisfy the statutory requirement to “address increasing available capacity to meet forecasted load,” instead relying on preexisting forecasts for new generation additions that do not include substantially more reliable generation in West Texas.

Neither ERCOT’s studies nor the PUC’s actions fully satisfy the statutory requirement to “address increasing available capacity to meet forecasted load,” instead relying on preexisting forecasts for new generation additions that do not include substantially more reliable generation in West Texas (ERCOT, 2024, p. 5). Given that there is no region of the state where reliable capacity currently exceeds demand (p. 11), the plan assumes that new generation will be built in other parts of the state to provide the “import capacity” to West Texas. That new capacity could be built in West Texas, but the PBRP says that it won’t happen under current market conditions. The PBRP is fundamentally a “build transmission first and hope the generation comes after it” approach to the reliability problems in the region.

Another piece of information missing from these studies is the consumer cost savings test, which the Texas Legislature mandated in 2021 (SB 1281, 2021) and the PUC finalized at the end of 2022 (16 TAC §25.101). By rule, either ERCOT or the applying TSP must show that the congestion cost savings for a project are “equal to or greater than the average of the first three years annual revenue requirement” (16 TAC §25.101(a)(3)(A)(i)(I)(-a-)). In other words, the PUC will not approve a CCN for a new project unless it passes an economic cost-benefit test for consumers. This test can be bypassed for “projects deemed critical to reliability” by ERCOT, and those projects must be approved within 180 days instead of the usual 360 days (16 TAC §25.101(a)(3)(D)). HB 5066 essentially gave ERCOT the ability to deem all the 765-kV STEP as critical to reliability and thereby expedite the approval process. One purpose of this study is to fill in this gap and to assess the economic costs and benefits of the 765-kV STEP.

LOAD FORECASTING AND TRANSMISSION PLANNING FOR THE PERMIAN BASIN

The PBRP was preceded by two transmission planning studies (ERCOT, 2019; ERCOT, 2021) from ERCOT and three different load forecasting studies from Oncor/IHS Markit (IHS Markit, 2020), the University of Texas Bureau of Economic Geology (BEG) (Lin et al., 2022), and S&P Global (Zoba et al., 2022). Oil and gas producers frustrated by the slow pace of improvements and long interconnection wait times were the primary motivators behind HB 5066 (as evidenced by the witness list for the bill, see HB 5066, 2023b), which allowed ERCOT and the PUC to forego the regular piece-by-piece process and approve a whole suite of projects en masse.

The PBRP is unique from these prior studies in calling for long-distance transmission to import power into the region. The only other study ERCOT performed that considered transmission similar to the 765-kV lines was its Long-Term West Texas Export Study (ERCOT, 2022), which was designed to move wind and solar out of West Texas. That study contemplated four long-distance lines—the southern three of which align roughly with the 765-kV lines in the PBRP (p. iv)—and considered voltages above the existing 345-kV export lines. Despite the export study being published in January 2022, just months before the S&P study that formed the foundation for the PBRP, it did not consider the import potential of the lines. In fact, it notes that east-to-west flows were only occurring about 10% of the time across the existing lines in its 2023 model (p. 5).

If one examines the body of literature prior to the PBRP, it is hard to avoid concluding that the 765-kV lines in the PBRP are designed as much to integrate more wind and solar across the entire ERCOT grid as they are to import power into West Texas. Prior to the S&P study, only local transmission upgrades were being considered to serve oil and gas loads in the region, not the long-distance lines. Regardless of the motivation, the Long-Term West Texas Export Study is further evidence that if not for the overbuilding of wind and solar in West Texas, ERCOT probably would never have considered the current 765-kV lines to that region.

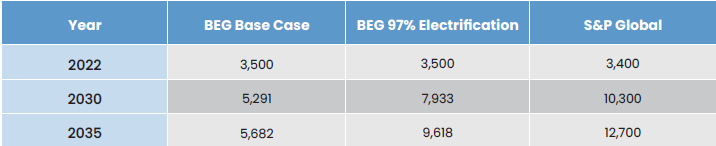

The reason ERCOT shifted toward building import lines instead of export lines was a large increase in its demand forecasts for oil and gas production and computing in West Texas. When developing the PBRP, ERCOT chose to ignore the BEG study, which ERCOT commissioned itself, and to rely solely on the S&P study, commissioned by six of the oil and gas companies—Chevron, ConocoPhillips, Devon Energy, Diamondback Energy, ExxonMobil, and Pioneer Natural Resources—that were lobbying for more transmission upgrades. In fact, the PBRP offers a comparison of different demand forecasts for the region but does not even mention the BEG study (ERCOT, 2024, p. 9). This choice was consequential because the S&P projections for electricity demand from oil and gas production by 2035 are more than twice the median projection in the BEG study.

Table 2

2030 Comparison of Electricity Demand Forecasts for Oil and Gas Production in the Permian Basin, in MW

Note: Data from (https://www.ercot.com/files/docs/2022/06/10/ERCOT_West_Texas_Load_Study_Report.pdf), p. 5, and (https://www.ercot.com/files/docs/2023/03/17/Presentation%20to%20ERCOT%20planning.pdf), p. 26.

The primary driver of these differences, as noted by S&P in its comparison of the two studies (S&P Global, 2023, p. 35), is how much each study assumes oil and gas companies will pursue electrification to reduce emissions. The BEG study predicts 9.6 GW of oil and gas demand by 2035 in its high electrification case, (Lin et al., 2022, p. 5), and its highest predictions approach the 12.7 GW predicted by S&P (Zoba et al., 2022, p. 26). Most of the demand in the high electrification scenarios comes from converting gas lift, gathering, and processing activities from gas generators to grid power. In other words, many of the large transmission projects planned for the region (including the 765-kV import lines) might be avoided entirely if oil and gas producers chose to continue relying on the gas and diesel generators they currently use. The new lines are not essential for continued oil and gas production, but rather for the emissions reductions plans that producers are pursuing.

ERCOT’s latest long-term load forecast shows only about 3.1 GW of new oil and gas loads by 2030 (ERCOT, n.d.-a), substantiating our hypothesis that the S&P Global forecast was overwrought. From a transmission planning standpoint, the fact that demand from oil and gas production will likely never reach the levels forecast in the S&P study has been overtaken by the dramatic increase in projected computing loads in the region. However, the PBRP was sold to policymakers as essential to meeting critical oil and gas loads, thereby justifying the substantial landowner impacts of the 765-kV lines and socializing the costs to all ratepayers. If the 765-kV lines are solely needed to meet new data center demand and emissions reduction goals, then the need for the lines and how their cost is allocated must be subjected to greater scrutiny.

ERCOT’s Long-Term West Texas Export Study is further evidence that if not for the overbuilding of wind and solar in West Texas, ERCOT probably would never have considered the current 765-kV lines to that region.

THE 765-KV STEP IS A CHOICE, NOT A NECESSITY

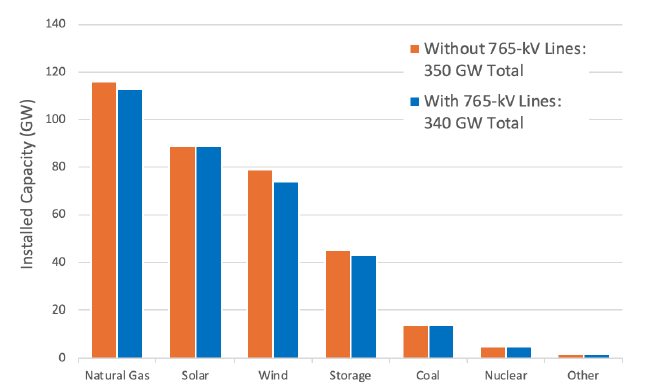

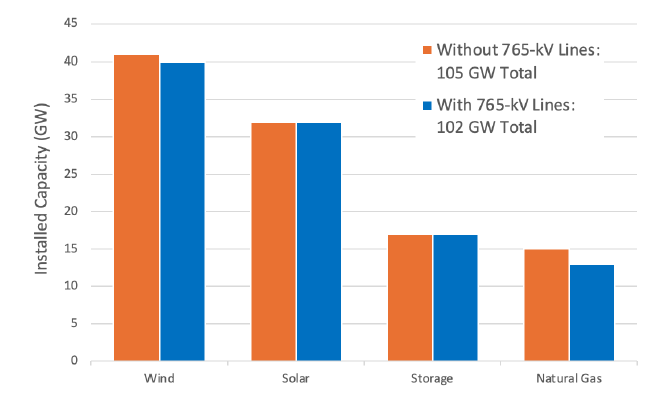

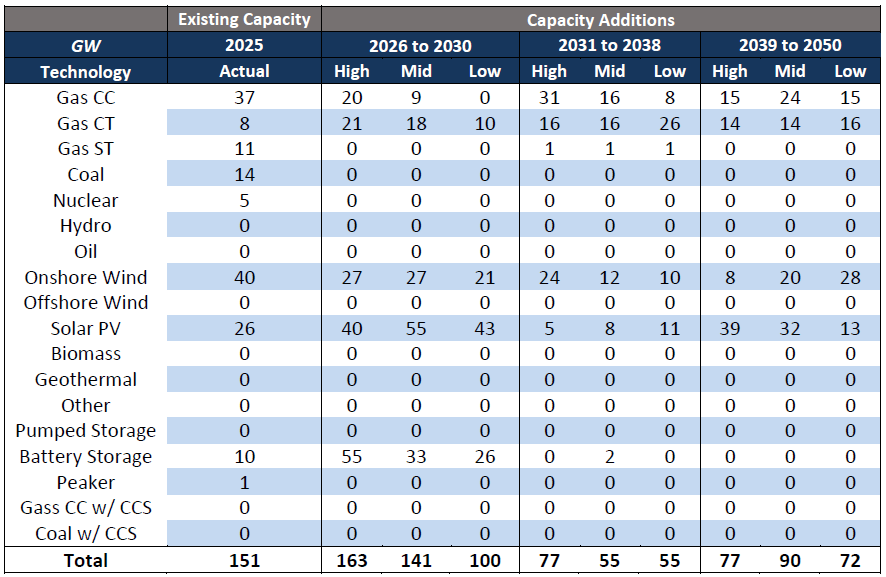

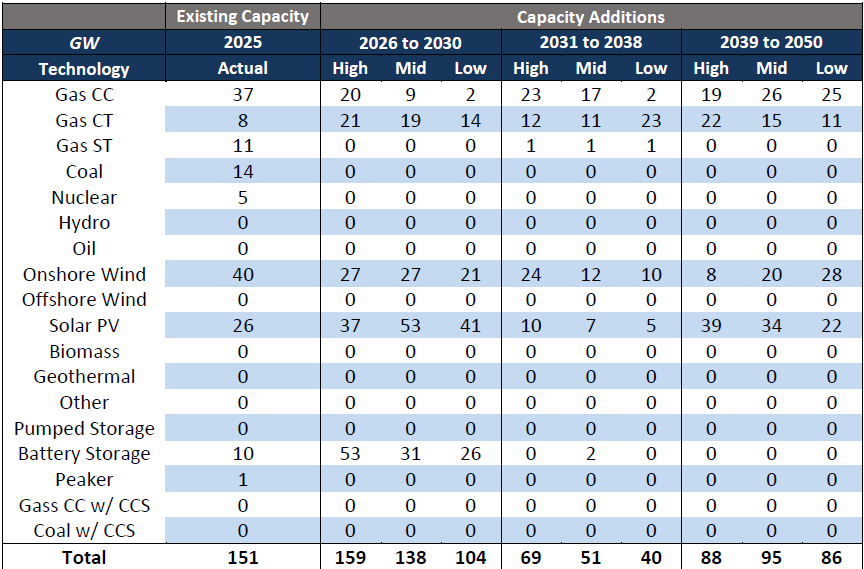

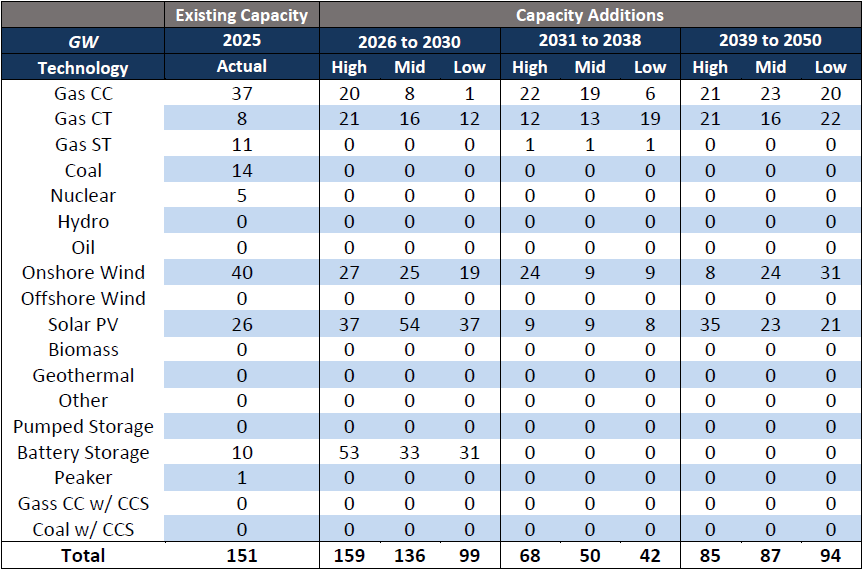

The attached study from Energy Ventures Analysis (EVA) provides further evidence that the 765-kV STEP is a choice, not a necessity, and that other policy choices can enable the 765-kV lines to be avoided entirely. Setting aside the optionality data centers have and assuming all regions of the state experience significant demand growth over the next decade, the study finds that the lines do not change the overall generation mix materially. In the mid-demand cases (i.e., 2038 systemwide peak demand of 148 GW) with and without the 765-kV lines, the amount of generation capacity in ERCOT will more than double by 2038, from 151 GW in 2025 to 340-350 GW in 2038. As shown in Figures 3 and 4, the 765-kV lines only reduce the total amount of new generation needed in ERCOT by 10 GW, or about 3%, and they only reduce the amount of new gas generation in West Texas by 2 GW.

Figure 3

Installed Capacity by Resource Type in ERCOT in 2038 With and Without the 765-kV Lines

Note: Data from Evaluating the Cost of ERCOT’s Permian Basin Reliability and Strategic Transmission Expansion Plans, Energy Ventures Analysis, May 2026, p. 17-18. This data is from the mid-demand case.

Figure 4

Installed Capacity by Resource Type in West Texas in 2038 With and Without the 765-kV Lines

Note: Data from Evaluating the Cost of ERCOT’s Permian Basin Reliability and Strategic Transmission Expansion Plans, Energy Ventures Analysis, May 2026, p. 19. This data is from the mid-demand case.

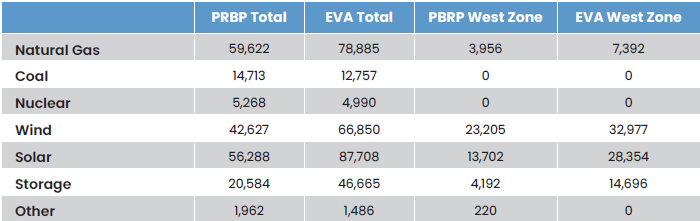

Table 3

2030 Installed Capacity by Fuel Source, PBRP vs. EVA Study Mid-Demand Scenario, in MW

Note: PBRP data derived following the instructions described in Section 2.1.3 in the PBRP, see ERCOT Permian Basin Reliability Plan Study, Electric Reliability Council of Texas, July 2024, pp. 5-6 (https://interchange.puc.texas.gov/Documents/55718_17_1414013.PDF). EVA data taken from the cases without the 765-kV lines (see pp. 17-19 of the EVA study).

The future generation mix in ERCOT is determined primarily by market design, access, and prices, and more long-distance transmission simply provides optionality for where to locate that generation. A key assumption in the EVA study is that federal subsidies for wind and solar end for units placed in service after 2029, as current policy dictates, and that current supply chain constraints for new gas generation are resolved over the next few years. A change in either assumption, in the absence of market reforms to support more reliable generation, could lead to a greater amount of wind and solar in ERCOT and the need for more transmission. The challenge is that more transmission does not ensure that enough new reliable generation will be built to meet demand and could even discourage such generation if the transmission provides wind and solar favorable market access.

It is important to emphasize that the need for the 765-kV lines is driven by ERCOT’s assumption that Texas will continue to experience overbuilding of wind and solar, leading to new gas generation being constrained.

It is important to emphasize that the need for the 765-kV lines is driven by ERCOT’s assumption that Texas will continue to experience overbuilding of wind and solar, leading to new gas generation being constrained. This assumption is based on the criteria ERCOT uses to incorporate new generation into its planning models, which build on the existing interconnection queue and extrapolate from it. That queue is still predominantly wind, solar, and storage (ERCOT, n.d.-a). As Table 3 shows, ERCOT’s criteria constrain both the quantity of generation and where that generation can be built, especially in West Texas, which forces ERCOT to rely more on transmission to balance the system. The EVA study demonstrates that building more generation assets closer to demand centers enables different outcomes in which new transmission is avoided. It also reflects the fact that demand forecasts and the need for more generation have increased substantially compared to when the PBRP data was compiled in 2024.

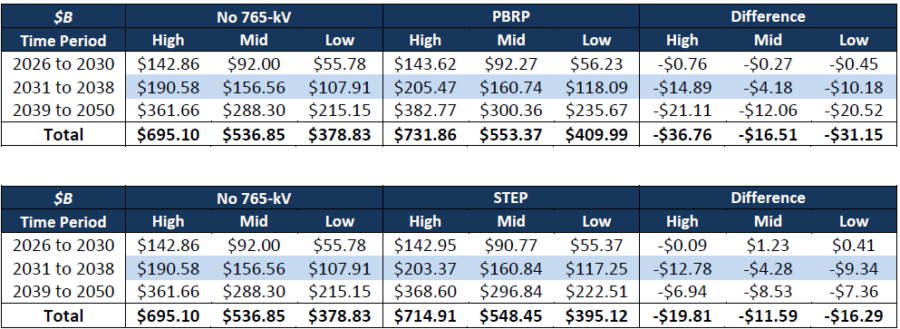

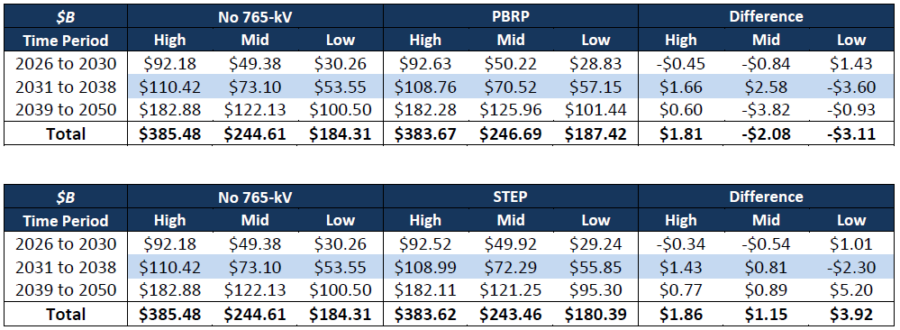

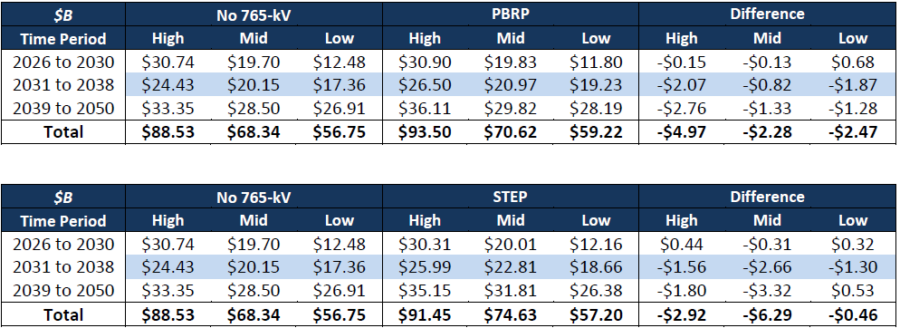

Table 4

EVA Study Average Annual Capital Expenditures and System Energy Costs from 2026 to 2038, Mid-Demand Scenario, in Millions of Dollars

Note: Data from the author’s calculations using the data from pp. 11-12 of the EVA study.

Because the 765-kV lines have little effect on the quantity and type of generation built in the EVA model, they also have little effect on total capital expenditures and on market prices. Under the EVA study’s mid-demand scenario, the 765-kV lines have no impact on transmission and generation spending while increasing annual energy costs by about $2 billion. These numbers are much smaller than the model error bounds and are highly sensitive to the type and quantity of generation built, as well as to whether there is enough total generation in the system to meet demand at all times.

The bottom line is that the 765-kV lines do not materially change the economic profile of the ERCOT market, and that the lines can be avoided without a significant impact on prices or reliability for consumers. The consumers who will be affected by the absence of the 765-kV lines are large industrial consumers and data centers seeking greater access to wind and solar power. For everyone else, what ultimately matters for cost and reliability is ensuring the system has enough affordable, reliable generation to meet demand. Transmission lines do not create power and cannot solve that problem.

THE 765-KV STEP SHOULD BE DELAYED AND REEVALUATED

The 765-kV STEP was developed and approved primarily because a wide array of entities stand to benefit from them, namely:

- Transmission companies: The most evident beneficiaries of new transmission are the companies that build the lines, which receive a guaranteed return on equity on their capital expenditures. Assuming the entire $33 billion 765-kV STEP is financed with a 50% debt-to-equity ratio and a 10% return on equity, the transmission companies will receive roughly $25 billion in equity returns (see Bennett & Piracci, 2026, pp. 19-20, for the cost-recovery methodology).

- ERCOT and PUC leadership: Since ERCOT and the PUC cannot control where load and generation are sited, new transmission is one of the only tools they have to manage reliability. Outages caused by transmission congestion or transmission failures, or slow interconnection times for new load or generation, also represent risks that they want to avoid.

- Power plant developers: Any entity that owns or builds power plants is not required to pay for new transmission under current market rules. New transmission lines are especially critical for wind and solar developers who need grid connections across broad swaths of land and high-capacity lines to handle the volume when they are operating at maximum capacity.

- New industrial consumers: This group may not seem like an obvious beneficiary, since the 765-kV lines significantly raise their transmission cost burden, but the new class of data centers cares more about grid access than marginal transmission costs. Also, many consumers seeking to meet net-zero emissions goals want to access wind and solar power via the grid rather than be forced to build on-site gas generation.

The influence of the net-zero goals and federal subsidy-driven actions of many industrial consumers bears emphasizing. Historically, industrial consumers represented by the Texas Association of Manufacturers have been opponents of increased transmission spending because they pay a large share of transmission costs and are highly price-sensitive. However, their representatives supported HB 5066 (2023b) and voted for the 765-kV STEP in the ERCOT stakeholder process (ERCOT, 2025d). Given the primary conclusion of this study—that the main effect of the 765-kV lines is to integrate more wind and solar into the ERCOT grid—it must be asked whether these companies are now supporting more transmission lines because they have decided to put greater priority on consuming more wind and solar power to leverage federal tax credits and pursue corporate sustainability goals.

Unlike the many stakeholders who will benefit from the 765-kV STEP, the people who will be harmed by it—the residential and small commercial ratepayers who will only see the pass-through costs and no market benefits, plus the landowners whose land is seized and devalued—had no direct say in the planning process prior to the CCN applications being filed. For most transmission projects, which do not come anywhere close to the statewide impact, substantial cost, and policy implications of the 765-kV STEP, the existing process is efficient and sensible. But the fact that a plan the size of the 765-kV STEP was instituted without any direct mandate from the Texas Legislature (in contrast to the CREZ lines that were expressly directed by legislation) is a profound mistake that must be corrected. Now is the time for the PUC to halt the CCN applications and allow the Legislature to consider the 765-kV STEP more carefully during the 2027 legislative session.

If the Legislature takes up the opportunity to reconsider the 765-kV STEP, it has four primary alternatives to choose from:

- Change nothing and let the market adjust to any transmission bottlenecks that occur in the absence of the 765-kV lines.

- Enact market reforms to better value reliable generation and to encourage that generation to locate closer to the demand.

- Directly subsidize gas generation in certain locations across the ERCOT grid to provide extra insurance against reliability issues.

- Require new data centers to be curtailed so that peak demand never rises above a level that outstrips transmission capacity.

The fact that a plan the size of the 765-kV STEP was instituted without any direct mandate from the Texas Legislature is a profound mistake that must be corrected. Now is the time for the PUC to halt the CCN applications and allow the Legislature to consider the 765-kV STEP more carefully during the 2027 legislative session.

These options can be pursued independently or through a combined approach. The primary conclusion of this study is that the 765-kV lines will not materially change the overall generation mix in ERCOT or reduce energy prices. Therefore, the Legislature can delay the lines while alternative options are pursued. What will make a material difference in the ERCOT market are changes in market design, and the Legislature should aggressively pursue market reform options first before allowing ERCOT and the PUC to move forward with the 765-kV STEP or any other statewide transmission plans.

Lawmakers will be tempted to pursue option #3, as evidenced by their creation of the Texas Energy Fund, because direct subsidies provide more certainty that new gas generation will be built and allow them to take credit for what does get built. But permanent subsidies will only exacerbate the central planning problems that led to the 765-kV lines. If the Texas Energy Fund is used for anything, it should be repurposed to protect residential and small commercial ratepayers from the coming increases in transmission and wholesale energy costs, spent down accordingly, and retired as soon as possible.

Option #4 is essentially an extension of the goals of SB 6, enforcing scarcity on one segment of consumers, data centers, to avoid pushing scarcity onto the rest of the grid. As a temporary measure to avoid another central planning problem, policies in this vein must be considered alongside policies to stop overbuilding wind and solar and to increase the supply of on-grid gas generation. ERCOT and the TSPs are already doing their own form of gatekeeping by instituting the batch study process and delaying interconnections for new data centers. Allowing data centers greater market access in exchange for operational flexibility, as proposed by Planning Guide Revision Request 134 (Sharma Frank, 2025), could be a more market-friendly policy than a strict mandate.

Regardless of which option or set of options is pursued, the 765-kV STEP and the massive growth in data center demand have combined to expose the fact that the ERCOT market must be reformed to serve ratepayers first and not special interests. Only the elected representatives of the people in the Legislature can ensure that this happens, and it is time for policymakers to roll up their sleeves and get to work.

REFERENCES

Bennett, B., & Piracci, J. (2026, January). The explosion of transmission costs in ERCOT: Causes, forecasts, and policy solutions. Texas Public Policy Foundation. https://www.texaspolicy.com/wp-content/uploads/2026/01/2026-01-LP-Transmission-Costs-BennettPiracci.pdf

Electric Reliability Council of Texas (ERCOT). (2019, December 23). ERCOT Delaware Basin load integration study report. https://www.ercot.com/gridinfo/planning

Electric Reliability Council of Texas (ERCOT). (2021, December 8). ERCOT Permian Basin load interconnection study report. https://www.ercot.com/gridinfo/planning

Electric Reliability Council of Texas (ERCOT). (2022, January 14). Long-term West Texas export study report. https://www.ercot.com/files/docs/2022/01/14/Long-Term-West-Texas-Export-Study-Report.pdf

Electric Reliability Council of Texas (ERCOT). (2024, July). ERCOT Permian Basin reliability plan study report. https://interchange.puc.texas.gov/Documents/55718_17_1414013.PDF

Electric Reliability Council of Texas (ERCOT). (2025a, January 27). 2024 regional transmission plan (RTP) 345-kV plan and Texas 765-kV strategic transmission expansion plan comparison. https://www.ercot.com/files/docs/2025/01/27/2024-regional-transmission-plan-rtp-345-kv-plan-and-texas-765-kv-strategic-transmission-expans.pdf

Electric Reliability Council of Texas (ERCOT). (2025b, December). ERCOT’s transmission planning process. https://www.ercot.com/files/docs/2025/08/12/ERCOT_Trending_Topic-Transmission-Planning-Process.pdf

Electric Reliability Council of Texas (ERCOT). (2025c, December 1). Item 14.1: Recommendation regarding AEP Texas, CPS Energy, Oncor and CNP Texas 765-kV STEP Eastern Backbone Regional Planning Group (RPG) Project. https://www.ercot.com/files/docs/2025/12/01/14.1-25RPG025-AEP-Texas-CPS-Energy-Oncor-and-CNP-Texas-765-kV-STEP-Eastern-Backbone-Project.pdf

Electric Reliability Council of Texas. (2025d, November 19). 2025 TAC 765 kV STEP Eastern Backbone Project ballot 20251119. https://www.ercot.com/calendar/11192025-TAC-Meeting

Electric Reliability Council of Texas (ERCOT). (2025e, December 23). Report on existing and potential electric system constraints and needs. https://www.ercot.com/files/docs/2025/12/23/2025-Report-on-Existing-and-Potential-Electric-System-Constraints-and-Needs.pdf

Electric Reliability Council of Texas (ERCOT). (n.d.-b). ERCOT 2025 long-term load forecast report. Retrieved May 20, 2026, from https://www.ercot.com/gridinfo/load/forecast

Electric Reliability Council of Texas (ERCOT). (n.d.-c). GIS_Report_April2026. Retrieved May 20, 2026, from https://www.ercot.com/mp/data-products/data-product-details?id=pg7-200-er

HB 5066. Enrolled. 88th Texas Legislature. Regular. (2023a). https://capitol.texas.gov/tlodocs/88R/billtext/pdf/HB05066F.pdf#navpanes=0

HB 5066. House Committee Report Version, witness list. 88th Texas Legislature. Regular. (2023b, May 11). https://capitol.texas.gov/tlodocs/88R/witlistbill/pdf/HB05066H.pdf

IHS Markit. (2020, April 6). West Texas forecasted load additions: Permian Basin. Oncor Electric Delivery Company LLC. https://www.ercot.com/files/docs/2020/11/27/27706_ERCOT_Letter_to_Commissioners_-_Follow-up_Status_Update_on_Permian….pdf

Lasher, W. (2014, August 11). The competitive renewable energy zones process. Electric Reliability Council of Texas. https://www.energy.gov/sites/prod/files/2014/08/f18/c_lasher_qer_santafe_presentation.pdf

Lin, N, McDaid, G., Yan, Q., Lu, Y., & Goodman, E. (2022, June 10). ERCOT West Texas load study. University of Texas at Austin Bureau of Economic Geology. https://www.ercot.com/files/docs/2022/06/10/ERCOT_West_Texas_Load_Study_Report.pdf

Public Utility Commission of Texas (PUC). (2024, October 7). Order approving the reliability plan for the Permian Basin region in Project No. 55718. https://interchange.puc.texas.gov/Documents/55718_52_1433300.PDF

Public Utility Commission of Texas (PUC). (2025, April 24). Second order approving the reliability plan for the Permian Basin region in Project No. 55718. https://interchange.puc.texas.gov/Documents/55718_109_1492424.PDF

Texas Administrative Code. (n.d.). Title 16, Part 2, Chapter 25, Rule 101: Certification criteria. https://ftp.puc.texas.gov/public/puct-info/agency/rulesnlaws/subrules/electric/25.101/25.101.pdf

S&P Global Commodity Insights (S&P Global). (2023, March 22). Electrifying the Permian Basin: Prepared for ERCOT planning committee. https://www.ercot.com/files/docs/2023/03/17/Presentation%20to%20ERCOT%20planning.pdf

SB 3. Enrolled. 87th Texas Legislature. Regular. (2021). https://capitol.texas.gov/tlodocs/87R/billtext/pdf/SB00003F.pdf

SB 20. Enrolled. 79th Texas Legislature. Regular. (2005). https://capitol.texas.gov/tlodocs/791/billtext/pdf/SB00020F.pdf

SB 1281. Enrolled. 87th Texas Legislature. Regular. (2021). https://capitol.texas.gov/tlodocs/87R/billtext/pdf/SB01281F.pdf

Sharma Frank, A. (2025). 134PGRR-01 Interconnection Studies Reform for Dispatchable Loads 110125 in PGRR 134: Key Documents (webpage). Electric Reliability Council of Texas. https://www.ercot.com/mktrules/issues/PGRR134#keydocs

Zoba, T., Smith, C., Rao, M., Hao, Y., Li, K., Allen, W., Zarea, M., Gallagher, S., & Alekseenko, M. (2022, December). Electrification of the Permian Basin. S&P Global. https://interchange.puc.texas.gov/Documents/55718_3_1340806.PDF

Evaluating the Cost of ERCOT’s Permian Basin Reliability and Strategic Transmission Expansion Plans

Prepared by: Energy Ventures Analysis

Download the full analysis here.

Introduction

In May 2023, the Texas House Bill 5066, authored by Representative Charlie Geren, mandated that the Public Utility Commission of Texas (PUCT) direct the Electric Reliability Council of Texas (ERCOT) to create a plan to address electricity demand growth in West Texas over the next decade. The anticipated load growth is driven by the electrification of oil and gas operations, the construction of large load data center facilities, and other industrial expansions. In December 2023, the PUCT formally issued the Permian Order to ERCOT. In July 2024, ERCOT presented a final report on the Permian Basin Reliability Plan (PBRP) to the PUCT. In September 2024, the PUCT approved ERCOT’s PBRP.

As it stands at the preparation of this report, the PBRP was adopted as part of ERCOT’s strategic transmission expansion plan (STEP). The PBRP includes several local transmission upgrades, the construction of three 765-kV transmission lines in ERCOT, and a cost estimate of ~$14 billion.1 In addition, the STEP includes two 765-kV transmission lines between the North and South zones of ERCOT. However, if demand growth does not materialize or is significantly lower than the current projected level, the 765-kV lines investment would result in billions of dollars in stranded assets.

The high price tag of the PBRP and STEP, as well as the lack of publicly available analysis of alternative plans, has prompted stakeholders to conduct their own independent analyses. In collaboration with the Texas Public Policy Foundation (TPPF), Energy Ventures Analysis (EVA) has evaluated alternatives to the PBRP and STEP. These alternatives evaluated the build-out of generation additions to meet growing demand as an alternative to the proposed 765-kV lines. The results show that future demand could be met without the 765-kV lines at a similar cost, and this will be explored in further detail throughout this report.

Methodology

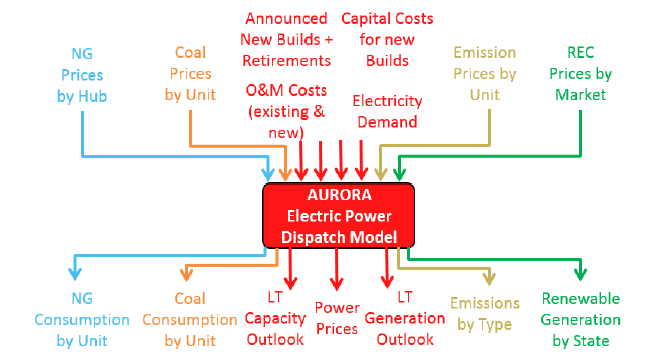

EVA’s energy forecasts are formulated using a bottom-up approach combining detailed market data and analysis with rigorous engineering principles. For example, EVA’s power team inputs its latest market research and analysis into the model. These inputs include electricity demand, capital costs for new market entrants by technology (e.g., combined cycle gas turbines (CCGT), simple cycle gas turbines (SCGT), wind, solar, storage, nuclear, coal with carbon capture and storage (CCS)), recently announced retirements and new builds, and future operation and maintenance (O&M) cost changes due to environmental retrofits, among others.

Model

EVA licenses the Aurora dispatch model from Energy Exemplar and has undergone an extensive customization process to repopulate the defaults with data from EVA’s own market research and insights. Some of the customizations include:

- Complete overhaul of grid-connected generating capacity based on the most recent Energy Information Administration (EIA) data and EVA’s proprietary Power Plant Tracking System

- Unit-specific scheduled and unscheduled maintenance outage rates based on historical performance

- Unit-specific heat rates based on historical performance and engineering principles

- Unit-specific emission rates based on historical performance and future emission control technologies

- Hourly utilization rates for solar and wind resources based on location and technology

- Unit-specific minimum up/downtime, ramp rates, and minimum load requirements based on historical performance and engineering principles

- Planning reserve margin requirements based on published Regional Transmission Organizations (RTO) and North American Electric Reliability Corporation (NERC) targets

- Capital cost, operational characteristics, and online dates for new entrants reflective of real-world data

EXHIBIT 1 shows key inputs and outputs of the Aurora electric dispatch model, the cornerstone of EVA’s integrated forecasts.

EXHIBIT 1: INPUTS AND OUTPUTS OF EVA’S AURORA ELECTRIC POWER DISPATCH MODEL

Other Inputs

Natural Gas Price Outlook

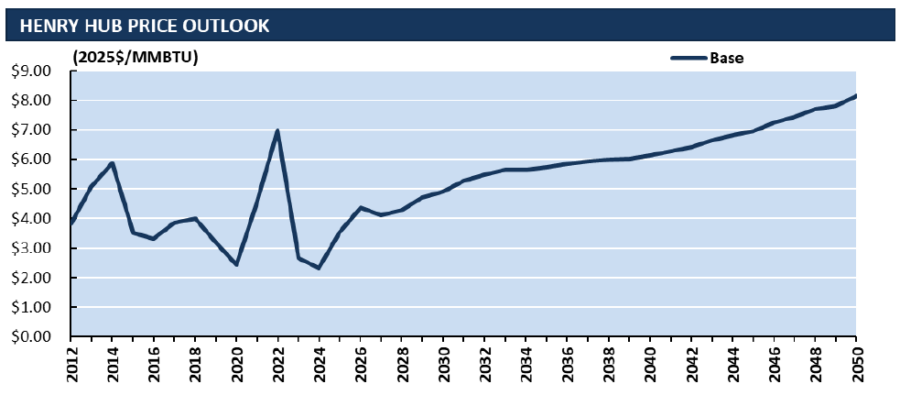

Henry Hub prices have been volatile, with the 2025-2026 winter season bringing sharp swings driven by weather events and record liquefied natural gas (LNG) feed gas demand. Near-term, prices are expected to remain in the mid-$3/MMBTU range through the injection season as storage inventories normalize from winter draws. Looking further out, EVA’s base case projects a materially higher price environment over the long term, with Henry Hub rising from the mid-$3s to levels above $8/MMBTU in real terms by 2050. This upward trajectory reflects a tightening market driven by accelerating electricity demand from data center growth and electrification, combined with sustained LNG export expansion pulling on domestic supply. Production responds but increasingly requires development in higher-cost pure-play gas basins, such as the Permian, drilled but uncompleted (DUC) backlog thins, and productivity gains plateau, lifting the marginal cost of supply over time.

Powder River Basin (PRB) Coal Price Outlook

PRB coal prices have been very stable since 2013, with the prompt-year forward market price (most PRB coal is purchased under annual contracts) for 8,800 Btu coal ranging from $11.00 to $15.00 per ton, over 80% of the time. Except for a 5-month period from September 2021 to January 2022, the forward price has never been above $17.10 per ton. The price spike in late 2021 was driven by a sharp increase in demand for PRB coal amid a jump in natural gas prices during the recovery from the COVID recession.

EVA projects PRB coal prices to remain stable, growing very slowly in constant 2025 dollars, and growing with inflation in nominal dollars. Except for short periods of imbalance between supply and demand, we project market prices for 8,800 Btu coal to be in the range of $15.00 – $17.00 per ton in constant 2025 dollars. Prices can drop below production costs for short periods when demand falls, forcing mines to reduce production, and can rise well above production costs during periods of a surge in demand. The primary driver of short-term swings in demand will be changes in winter weather, which affect the demand and price of natural gas, causing the economic dispatch of PRB power plants to vary coal burn in response.

Capital Costs for New Generation Units

EVA forecasts technology-specific capital costs for new builds by tracking current project costs, future changes in labor and materials costs, and relevant subsidies. For example, the federal tax credits for solar and wind resources have been updated to have an early expiration date under the One Big Beautiful Bill Act (OBBBA). The cost of required environmental upgrades is also included based on publicly available data and EVA estimates. EXHIBIT 2 provides the capital cost estimates incorporated into EVA’s analysis.

EXHIBIT 2: OVERNIGHT CAPITAL COSTS FOR DIFFERENT GENERATION TECHNOLOGIES THROUGH 2050

Representing the PBRP and the STEP

EVA’s license of the Aurora power dispatch model from Energy Exemplar also includes a long-term capacity expansion (LTCE) feature that enables the model to build new generation to meet future demand at the lowest system cost. This is an important difference between our analysis and ERCOT’s analysis. ERCOT’s PBRP report refers to the Generator Interconnection Status (GIS) report as the basis for generator additions. However, these additions were limited to commercial operation dates before 2030, despite the analysis period extending to 2038. In EVA’s analysis, the LTCE study period was 25 years (2026-2050). The EVA LTCE methodology provides a detailed understanding of the build-out of generation additions and the associated costs, with and without the 765-kV lines.

EVA ran an LTCE without any 765-kV transmission lines, a second LTCE with the planned 765-kV transmission lines for the PBRP, and a third LTCE with the planned 765-kV transmission lines for the STEP, comparing generation needs in each zone and the resulting cost impact. EVA performed this comparison for three different demand scenarios. This approach isolated the impact of the planned 765-kV transmission lines by keeping everything else constant and adding or removing only the 765-kV transmission lines. EVA modeled the PBRP 765-kV transmission lines as two 2,100 MW lines from North to West and one 2,100 MW line from South to West, coming online in 2031.2 EVA modeled the STEP 765-kV transmission lines as the three PBRP lines plus two 2,100 MW lines from North to South, coming online in 2031. The 765-kV transmission lines are configured to be bidirectional. An overview of the approved plan as proposed in the 2024 regional transmission plan is provided in EXHIBIT 3 below.3

EXHIBIT 3: MAP OF THE 765-KV STRATEGIC TRANSMISSION EXPANSION PLAN (STEP)

Scenarios

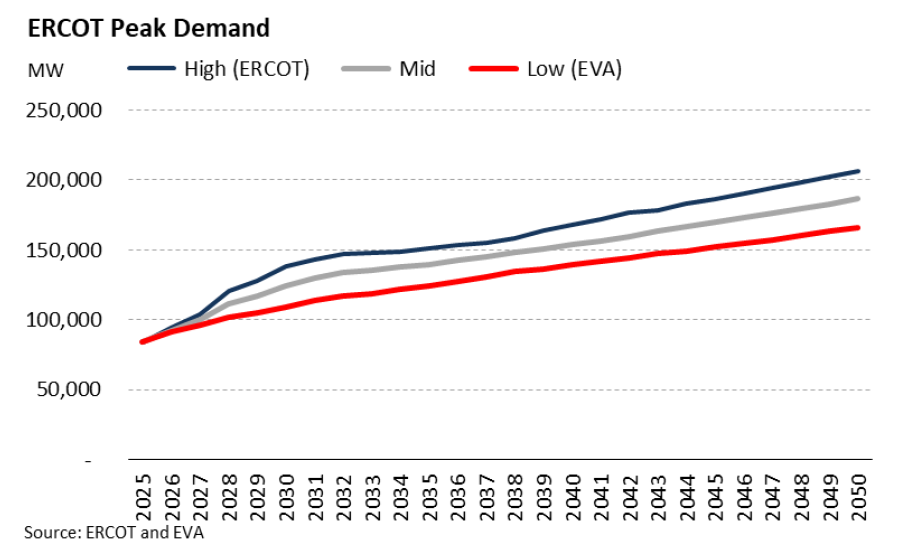

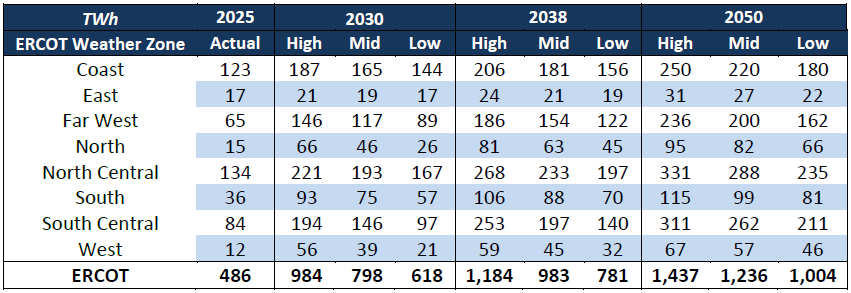

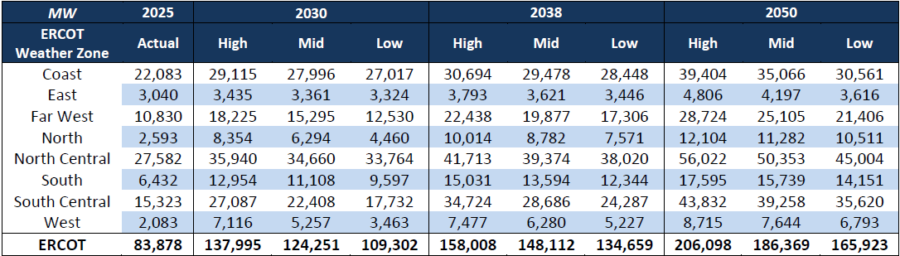

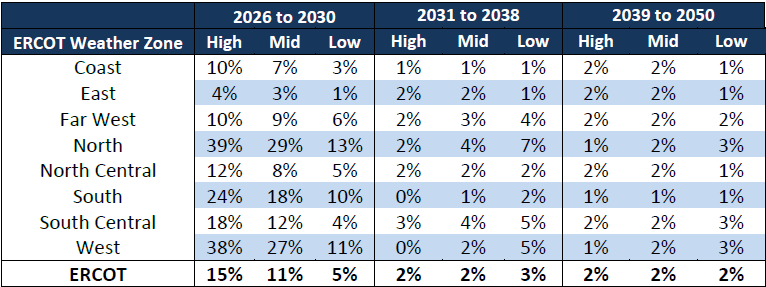

EVA compared three different demand scenarios for ERCOT, as shown in EXHIBIT 4, to analyze the impact of demand growth on the need for new generation, its cost implications, and to accurately quantify the risks. The first, referred to as the high case, utilized ERCOT’s 2025 hourly long-term energy forecast, which was directly input into the model.4 The second, referred to as the low case, uses EVA’s forecast, which is based on socioeconomics and a combination of other factors, including large loads, electrification, efficiency, and distributed generation. Finally, the third demand scenario, referred to as the mid case, represents the potential between the high and low cases. Much of the growth is expected to occur before the 765-kV lines come online in 2031. The only way to meet that demand would be with new capacity, unless the demand growth is delayed. EXHIBIT 5 shows that West demand remains a smaller share of total ERCOT demand than the North and South throughout the study period, even though, in the short term, West demand is growing faster.

EXHIBIT 4: ERCOT PEAK DEMAND THROUGH 2050

EVA uses a combination of state-level socio-economic factors, such as GDP, industrial production, employment, and disposable income, as inputs to advanced regression models to forecast electric demand by ISO zone, NERC sub-region, and major utility. In addition, EVA adds a layer of forecasts for distributed generation, energy efficiency, electrification of buildings and transportation, and data centers. Demand is further adjusted for normalized weather. Hourly demand shapes are also normalized from the last three to five years.

EXHIBIT 5: ERCOT TOTAL DEMAND BY WEATHER ZONE 5

EXHIBIT 6: ERCOT PEAK DEMAND BY WEATHER ZONE 6

Results

EVA compared the generation additions to meet demand without the 765-kV transmission lines, with the PBRP, and with the STEP before and after construction, keeping everything else constant. EVA then calculated the capital costs associated with the different generation additions. Finally, EVA also evaluated the impact on power prices and the potential benefits and savings available with alternative approaches to the 765-kV lines to meet demand.

Generation Additions

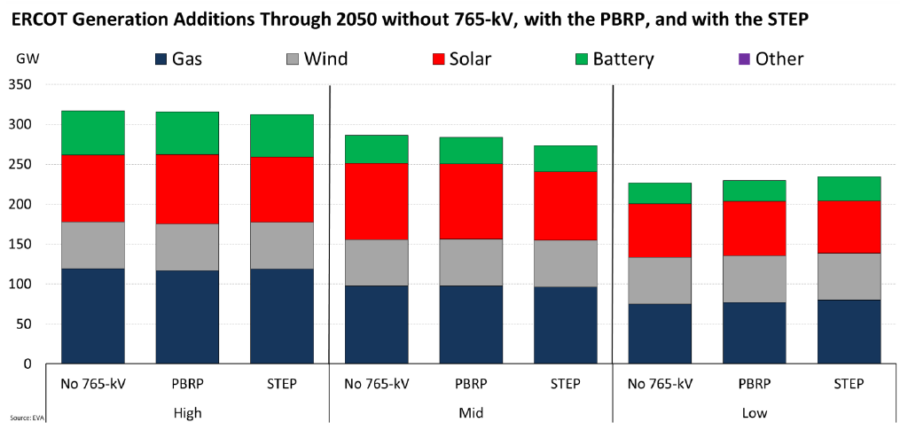

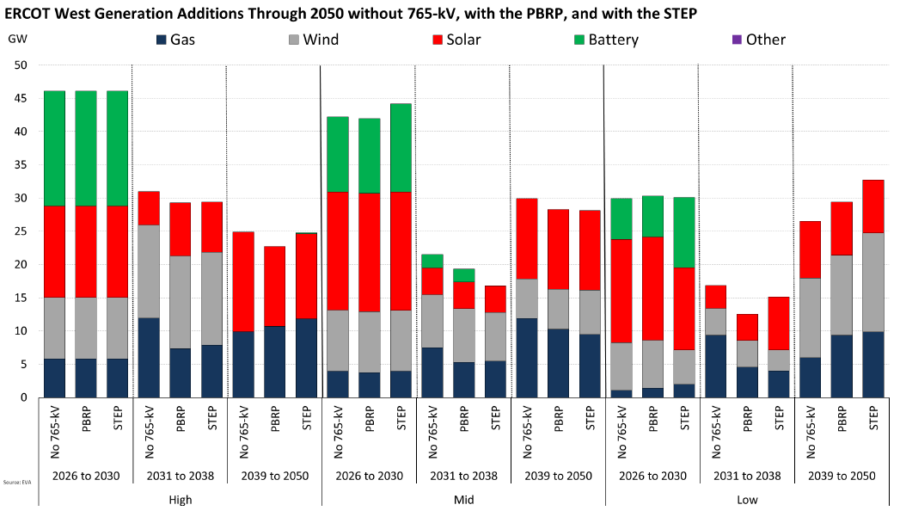

Existing generating capacity is generally distributed with renewable generation in West Texas and conventional generation near load centers in the North, South, and Houston. Traditionally, gas generation has not been built in the West because of fuel supply risk, a lack of load demand, low revenue because of no capacity payments and suppressed power prices with infrequent spikes from high renewable penetration that is consistently trapped locally because of congestion, and reliance on imported thermal generation from the North and South zones. However, the current demand outlook could significantly shift these dynamics. Gas generation additions could become favorable if around-the-clock demand materializes in the Permian Basin. In fact, extended interconnection timelines are prompting developers to pursue behind-the-meter generation across the country, especially in Texas, which could lead to demand growth overestimation and put the PBRP 765-kV lines at risk of becoming stranded assets.7

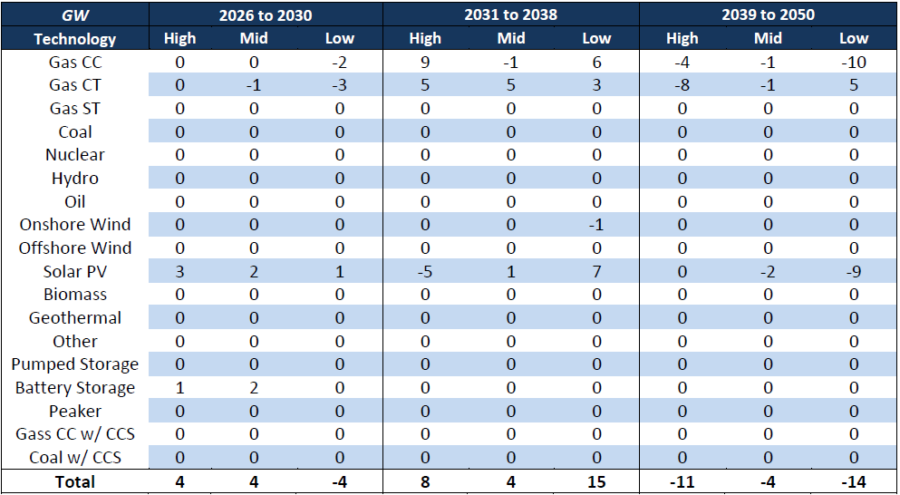

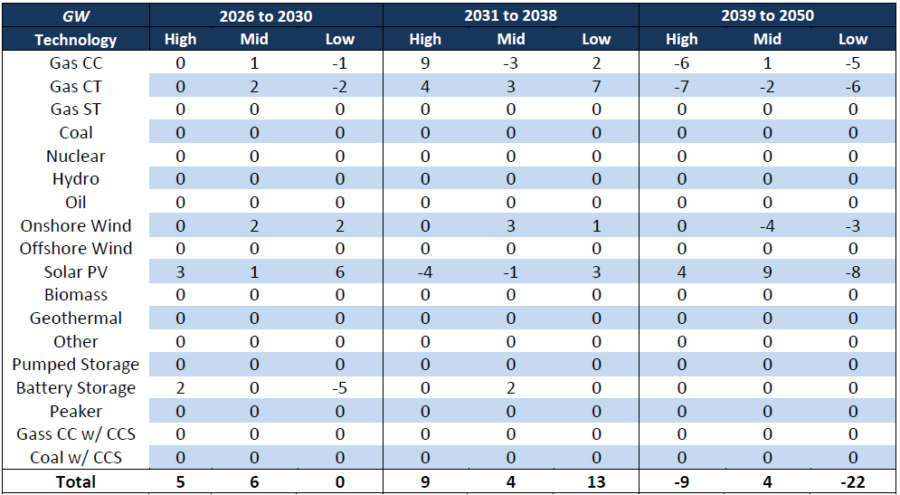

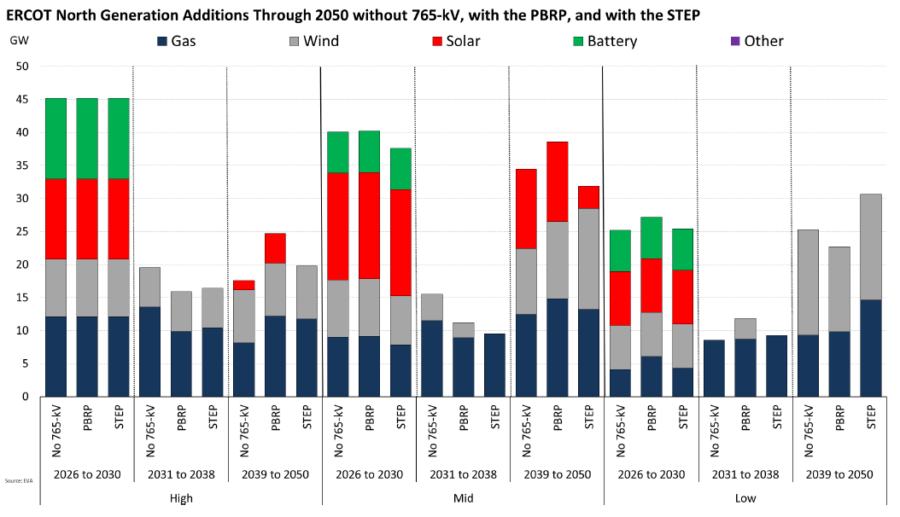

The 765-kV transmission lines do not reduce the need for generation by much for every demand case, as shown in EXHIBIT 7. On average, cases without the 765-kV transmission lines add ~5% more generation than cases with the PBRP and ~7% more generation than cases with the STEP by 2038. The more significant difference lies in where the generation is built, rather than how much is built. For example, in the high-demand case without the 765-kV transmission lines, the West zone adds ~4 GW more gas-fired capacity to meet growing demand compared with the case with the PBRP, which relies on more imports. We also observed that there are fewer gas steam turbine retirements across ERCOT zones in the high-demand case with the PBRP, primarily in the North, because these generators remain competitive for imports into the West. In the mid-demand case with the STEP, the North zone installs less solar than in the case without the 765-kV lines and relies more on imports from the South.

Renewable additions, especially solar, decline noticeably from 2031 to 2038 across all demand cases because they cannot meet evening demand peaks on their own. As previously mentioned, we project that federal production and investment tax credits (PTC and ITC) will expire by 2029, in line with the OBBBA, making renewables less competitive to build than gas until costs begin to decline organically. Dispatchable generation required to meet evening peaks creates a barrier to additional solar generation. Gas assets are more attractive than renewables because of low gas prices in West Texas, greater dispatchability driven by demand growth, and higher effective load-carrying capability (ELCC).

EXHIBIT 7: ERCOT GENERATION ADDITIONS THROUGH 2050 WITHOUT 765-KV, WITH THE PBRP, AND WITH THE STEP 8

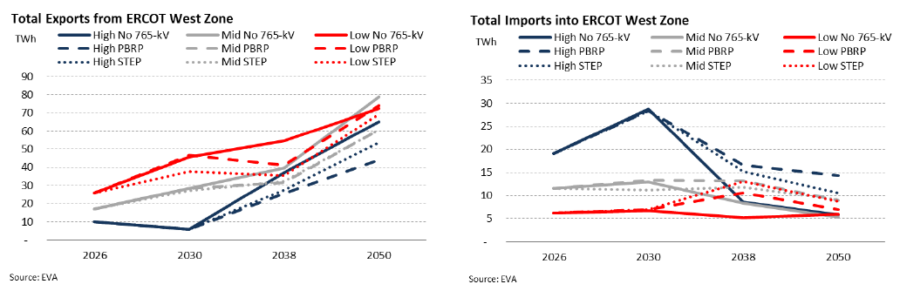

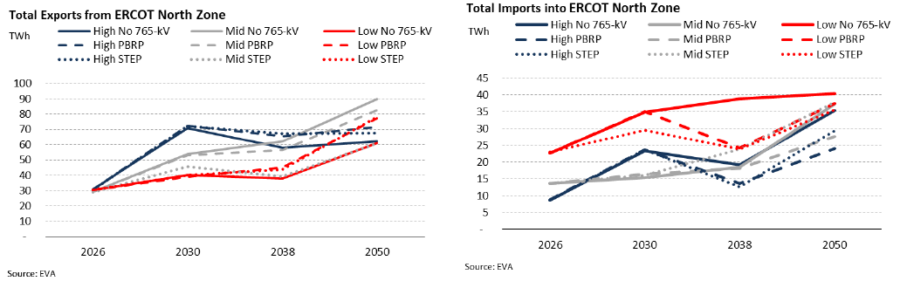

Transmission Utilization

Historically, West Texas has been a net power exporter of renewable generation, constrained by transmission capability. ERCOT’s long-term demand forecast suggests that the West zone interchange dynamics could be extended to include renewable exports to the Permian Basin and a greater reliance on thermal generation imports from the East during periods of low renewable generation. In the PBRP report, ERCOT noted that the 765-kV lines were designed with the Permian Basin’s and the overall ERCOT system’s needs in mind. ERCOT suggests that the PBRP could be used to import generation into the Permian Basin to serve forecasted load and to export renewable generation from West Texas to load centers in the East. However, demand in the West zone and ERCOT overall is expected to grow starting in 2026, while the 765-kV transmission lines are expected to come online in 2031. Since ERCOT is already constrained, the additional demand will require new generation to come online before 2030.

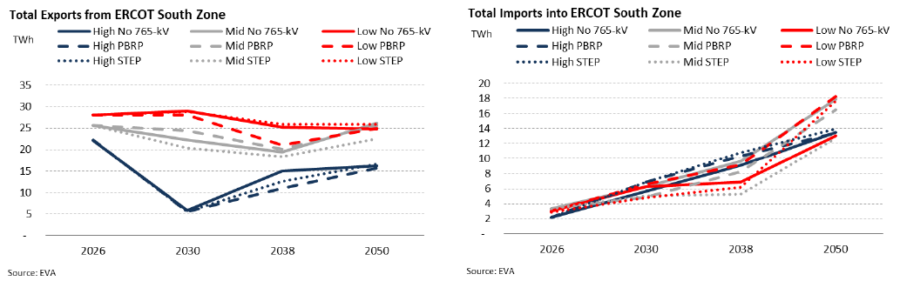

In our analysis, the 765-kV lines do not significantly change the zonal imports and exports, as shown in EXHIBIT 8. The West zone relies more on generation additions than on imports to meet growing demand. Not surprisingly, exports from the West zone, which is currently cited as a constraint, increase over time in all demand cases, but are lower with the 765-kV PBRP and STEP lines. Lower exports from the West zone in cases with the 765-kV transmission lines can be explained by higher generation additions and increased interchange between the North and South zones, eliminating the need for additional imports from the West. Imports into the West zone are higher when the 765-kV PBRP and STEP lines are included and change less over the study period, despite a significant near-term increase in the high-demand case. Exports from the North zone gradually increase over the study period and are generally higher with the 765-kV PBRP and STEP lines. Imports into the North zone gradually increase and are lower with the 765-kV transmission lines. In the low case, higher exports from the West zone balance higher imports into the North zone. Exports from the South zone significantly drop in the high case to accommodate local load growth, but remain stable in the other cases. Exports from the South zone are lower with the 765-kV PBRP and STEP lines. Imports into the South zone gradually increase with minimal difference when the 765-kV lines are included. In general, the differences in zonal exports and imports with and without the 765-kV transmission lines are minimal. This suggests that utilization rates decline in cases with the 765-kV transmission lines, as transmission capacity increases without a significant increase in import or export volumes.

EXHIBIT 8: ZONAL IMPORTS AND EXPORTS WITHOUT 765-KV, WITH THE PBRP, AND WITH THE STEP

Capital Costs

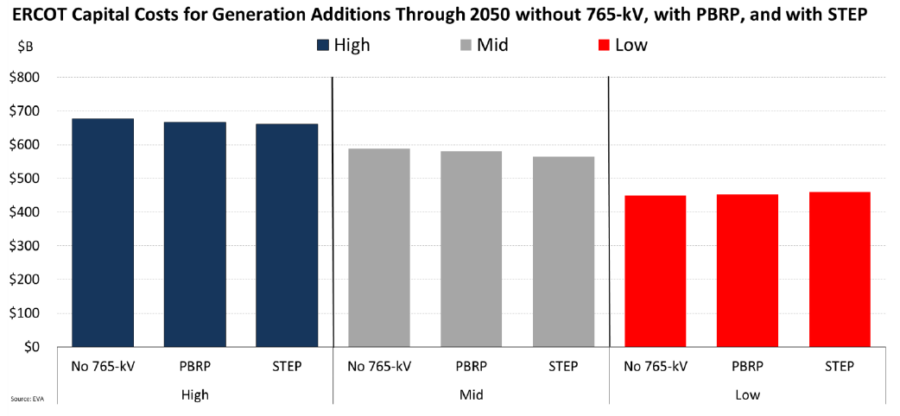

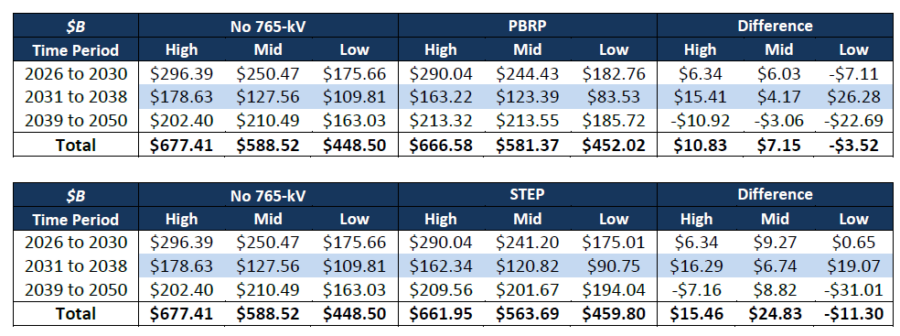

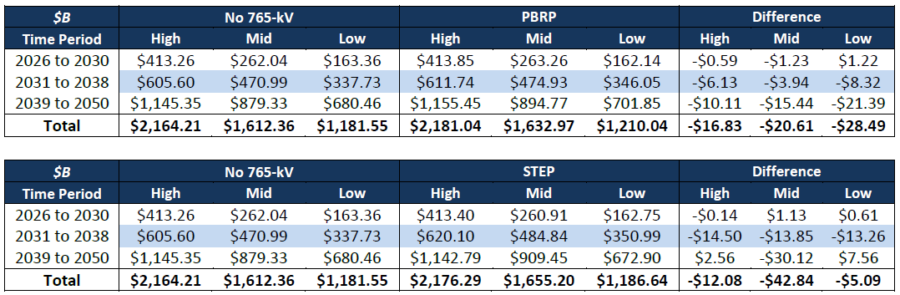

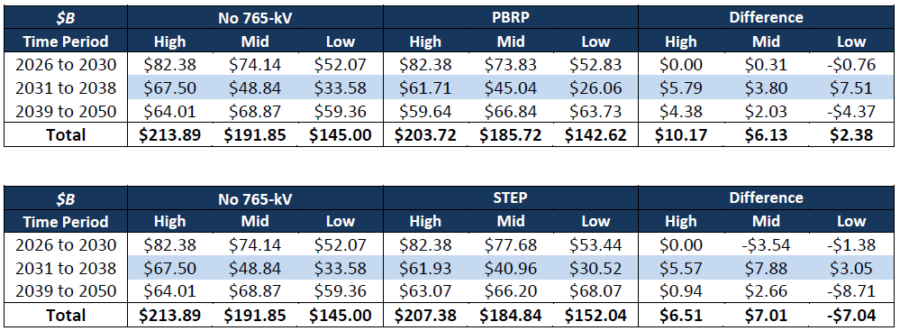

EVA calculated the capital costs associated with the generation additions based on the estimates provided in EXHIBIT 2. EXHIBIT 9 provides a summary of the capital costs associated with generation additions across the different demand cases, without 765-kV lines, with the PBRP, and with the STEP, throughout the entire study period. The increase in generation additions across the three cases without the 765-kV lines resulted in a ~5% increase in cumulative capital costs by 2038 for both the PBRP and the STEP. If the cost estimates for the 765-kV lines are included ($9B for the PBRP and $17B for the STEP), the increase is only ~2%.

EXHIBIT 9: TOTAL ERCOT CAPITAL COSTS 9

System Energy Costs

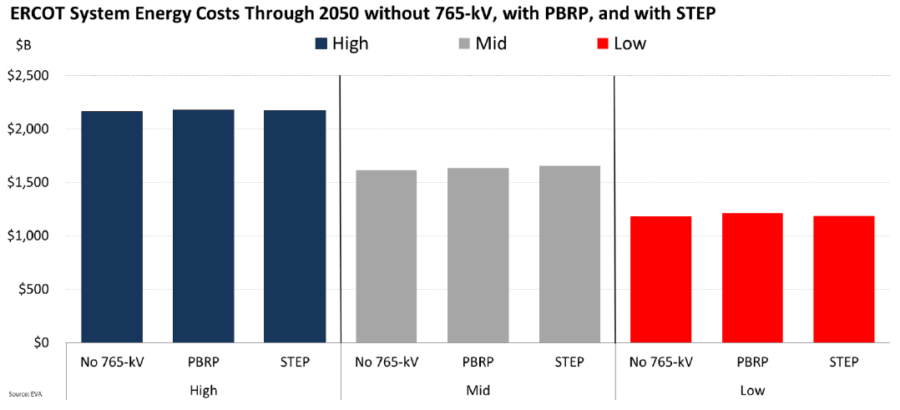

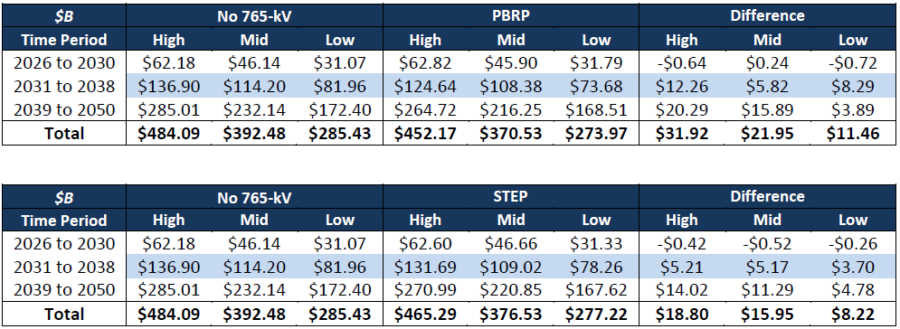

EVA also calculated system energy costs based on the difference in zonal power prices between the cases without 765-kV lines, with the PBRP, and with the STEP.10 The PBRP 765-kV lines result in slightly higher power prices in the North and South zones because they supply power to the West zone during higher-priced hours. Prices in the West zone also decline slightly due to increased imports from the North and South zones. These changes are only a couple of dollars per MWh annually. The effects of the PBRP on power prices are dampened by the full STEP, which increases interchange between the North and South zones.

EXHIBIT 10 provides a summary of the system energy costs associated with generation across different demand cases with and without the 765-kV lines throughout the entire study period. The cases without the 765-kV lines result in ~1% decrease in system energy costs by 2038.

EXHIBIT 10: DIFFERENCE IN SYSTEM ENERGY COSTS WITHOUT 765-KV, WITH THE PBRP, AND WITH THE STEP 8

Conclusions

In addition to local transmission upgrades and 765-kV transmission lines between the North and South zones, ERCOT’s STEP adopted the PBRP, a plan to ensure the Permian Basin has access to power to support growing demand by constructing three 765-kV transmission lines to increase renewable power interchange from West to East, a widely recognized existing system constraint. However, the potential benefit of these 765-kV lines is uncertain given the range of future outcomes. For example, much of the demand growth is projected to occur before the 765-kV lines are expected to come online in 2031. The only way to meet that demand would be to add new capacity, unless demand growth is delayed. Additionally, the growing demand in the Permian Basin will provide additional load to be served by excess renewable power, reducing the need for additional transmission from West to East. In contrast, a rising interest in behind-the-meter generation, driven by long interconnection timelines, could mean demand does not materialize, eliminating the need for 765-kV transmission lines.

Our analysis evaluated changes in long-term capacity expansion without 765-kV transmission lines, with the PBRP, and with the STEP. We found that generation additions were only ~5% to 7% higher by 2038 in cases without the 765-kV transmission lines, keeping everything else constant. Furthermore, the expected demand growth is creating a case for gas in the West as dispatchability increases and tax credits for renewables expire. In cases involving the 765-kV PBRP and STEP lines, utilization rates generally decline as transmission capacity increases, without a significant increase in import or export volumes. The increase in generation additions across the cases without 765-kV transmission lines resulted in a ~2% increase in cumulative capital costs by 2038, including the respective $9B and $17B cost estimates for the PBRP and STEP 765-kV lines, respectively. Furthermore, the cases without the PBRP and STEP 765-kV lines result in a ~1% decrease in system energy costs by 2038. Once the PBRP 765-kV lines are built, power prices in the North and South zones increase because they supply power to the West zone during higher-priced hours. Prices in the West zone also slightly decline due to increased imports from the North and South zones. These changes are only a couple of dollars per MWh annually. The full STEP mitigates the impact on power prices by increasing interchange between the North and South zones. The difference in capital and system energy costs by 2038, including estimated costs for the proposed 765-kV lines, is negligible, whether or not the 765-kV lines are included, suggesting that the proposed 765-kV lines do not provide a meaningful benefit to the ERCOT system.

Appendix

Detailed Assumptions

EXHIBIT 11: HENRY HUB PRICE OUTLOOK

EXHIBIT 12: TOTAL DEMAND CAGR FOR ERCOT WEATHER ZONES

ERCOT Maps 11

EXHIBIT 13: ERCOT LOAD ZONES

EXHIBIT 14: ERCOT WEATHER ZONES

ERCOT Generation Additions

EXHIBIT 15: TOTAL ERCOT GENERATION ADDITIONS WITHOUT 765-KV LINES

EXHIBIT 16: TOTAL ERCOT GENERATION ADDITIONS WITH THE PBRP

EXHIBIT 17: TOTAL ERCOT GENERATION ADDITIONS WITH THE STEP

EXHIBIT 18: DIFFERENCE IN TOTAL ERCOT GENERATION ADDITIONS (NO 765-KV MINUS PBRP)

EXHIBIT 19: DIFFERENCE IN TOTAL ERCOT GENERATION ADDITIONS (NO 765-KV MINUS STEP)

EXHIBIT 20: ERCOT WEST GENERATION ADDITIONS THROUGH 2050

EXHIBIT 21: ERCOT NORTH GENERATION ADDITIONS THROUGH 2050

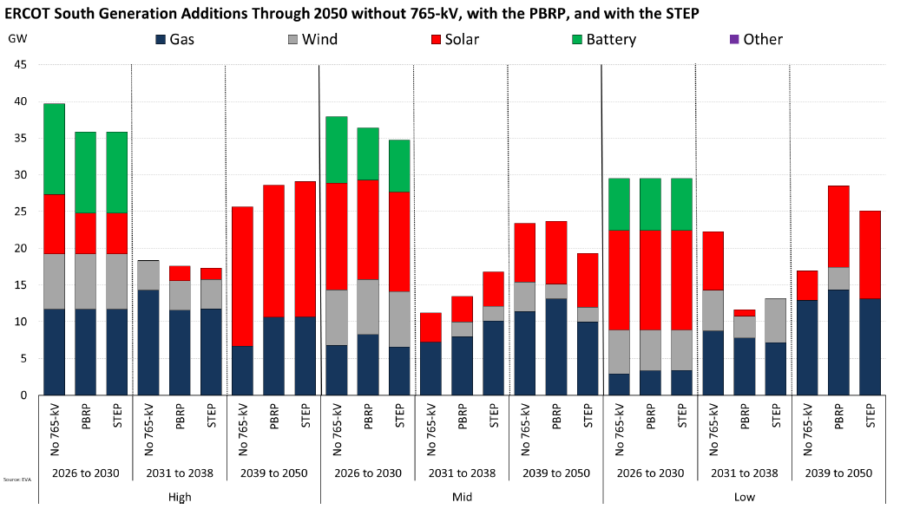

EXHIBIT 22: ERCOT SOUTH GENERATION ADDITIONS THROUGH 2050

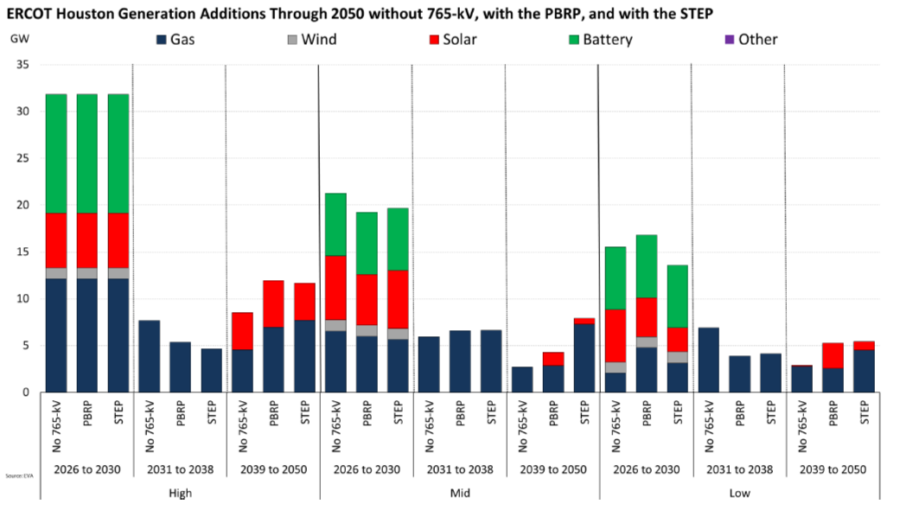

EXHIBIT 23: ERCOT HOUSTON GENERATION ADDITIONS THROUGH 2050

ERCOT Zones Capital Costs

EXHIBIT 24: ERCOT WEST ZONE CAPITAL COSTS

EXHIBIT 25: ERCOT NORTH ZONE CAPITAL COSTS

EXHIBIT 26: ERCOT SOUTH ZONE CAPITAL COSTS

EXHIBIT 27: ERCOT HOUSTON ZONE CAPITAL COSTS

EXHIBIT 28: ERCOT WEST ZONE SYSTEM ENERGY COSTS

EXHIBIT 29: ERCOT NORTH ZONE SYSTEM ENERGY COSTS

EXHIBIT 30: ERCOT SOUTH ZONE SYSTEM ENERGY COSTS

EXHIBIT 31: ERCOT HOUSTON ZONE SYSTEM ENERGY COSTS

EXHIBIT 32: ERCOT OTHER ZONES SYSTEM ENERGY COSTS

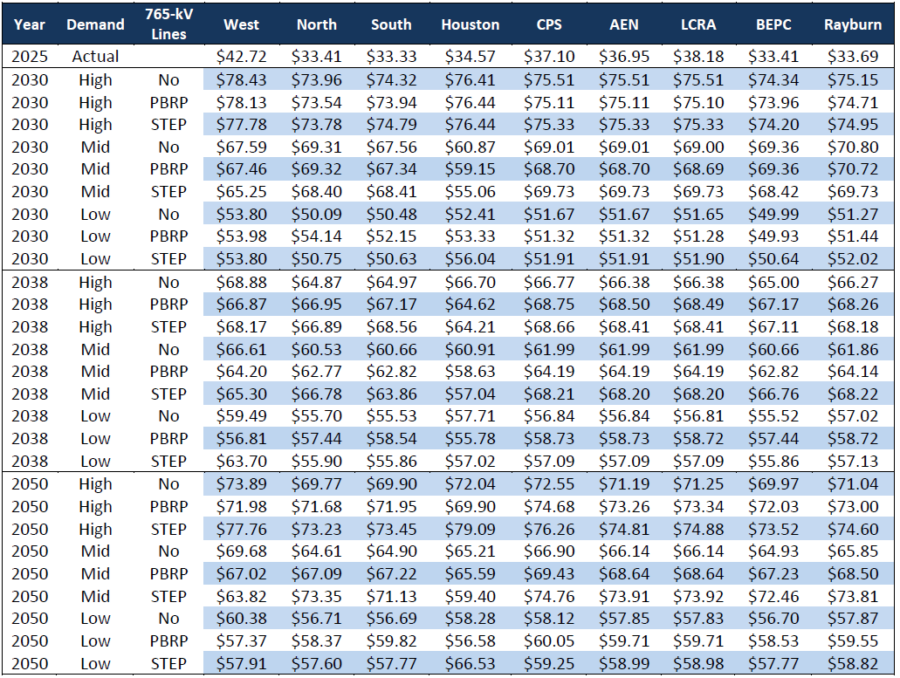

Power Prices

EXHIBIT 33: POWER PRICES ($/MWH) BY ERCOT LOAD ZONE