Texas’s business franchise tax is costly, complicated, and time-consuming to observe. Its negative and distortionary effects should motivate policymakers to eliminate it entirely.

Key points:

- Because of the substantial costs, large and small business owners can often spend more on compliance than on paying the franchise tax itself.

- Phasing out or repealing the tax altogether has the potential to create thousands of new jobs and add billions in additional personal income.

- In 2023, state lawmakers passed legislation that doubled the amount of revenue exempt from the tax, greatly expanding the number of businesses spared.

“This is the appropriate thing to do, to eliminate this bad tax.”

~ Former Texas House Ways & Means Chairman and Speaker of the House Dennis Bonnen, 2017

Issue

Texas’ business franchise tax, also known as the “margins tax,” is levied annually on certain taxable entities “conducting business in Texas, with exceptions for sole proprietorships, general partnerships directly owned only by individuals and their estates, and passive entities” (Legislative Budget Board, 2020, p. 2). Per the Texas Comptroller of Public Accounts (n.d.-b), entities subject to the franchise tax include:

- corporations;

- limited liability companies (LLCs), including single-member LLCs (SMLLCs) and series LLCs;

- banks;

- state limited banking associations;

- savings and loan associations;

- S corporations;

- professional corporations;

- partnerships (general, limited and limited liability);

- trusts;

- professional associations;

- business associations;

- joint ventures; and

- other legal entities.

To determine an entity’s taxable margin, the liability is the lesser of these four calculations: “(1) 70.0 percent of total revenue; (2) total revenue minus costs of goods sold; (3) total revenue minus compensation and benefits; or (4) total revenue minus $1.0 million” (Legislative Budget Board, 2025, p. 32). In 2026 and 2027, most entities will pay a tax rate of 0.75% of their taxable margin. One exception applies to entities primarily engaged in retail or wholesale trade, which are subject to a tax rate of 0.375% (Texas Comptroller of Public Accounts, n.d.-c). Thus, in order to ascertain what a business owes for any given tax year, the owner must engage with a set of complex calculations, determine the lowest value, and multiply that amount by one of two tax rates, depending on industry type. Depending on the size and nature of the business in question, this exercise can range from modestly difficult to daunting.

In some instances, certain taxable entities are exempt from paying the tax. In 2023, the 88th Texas Legislature established a No Tax Due Threshold for taxable entities whose annualized total revenues were equal to or less than $2.47 million, which had the effect of releasing “67,000 small to medium-sized [businesses] from paying the franchise tax” (SB 3 Bill Analysis, 2023, p. 1). This threshold remained fixed for the 2025 report year and increased to $2.65 million for 2026 and 2027 (Texas Comptroller of Public Accounts, n.d.-a).

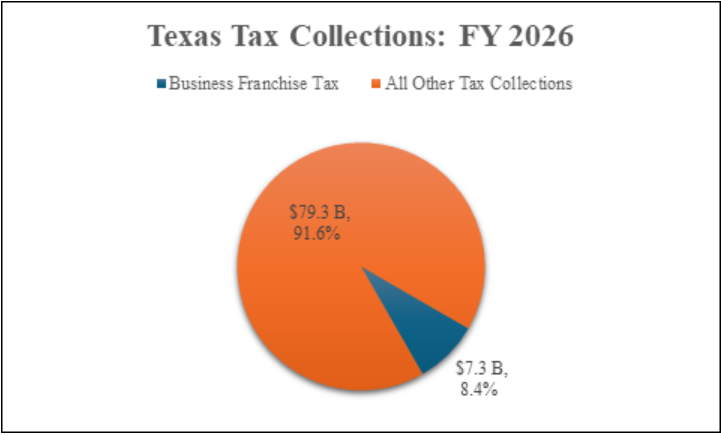

In the context of the state’s $338.2 billion budget for the 2026-27 biennium, the franchise tax generates a relatively modest amount of revenue, despite exemptions for certain entities. In fiscal years (FYs) 2026 and 2027, the tax is projected to yield $7.3 billion and $7.4 billion, respectively (Legislative Budget Board, 2025, p. 30). Franchise tax revenue is projected to be 8.4% of all tax collections in FY 2026 (see Figure 1). The franchise tax is the state’s second-largest tax revenue source, behind only the state sales tax, $51.1 billion in FY 2026, and just ahead of the motor vehicle sales and rental tax, $7.1 billion in FY 2026 (Legislative Budget Board, 2025, p. 30). As a percentage of all state revenue projected for FY 2026, franchise tax collections are expected to represent 4.1% of tax and nontax sources (Legislative Budget Board, 2025, p. 30).

Figure 1

State Revenue Comparison, Franchise Tax vs. All Other Tax Revenue, FY 2026

Source: Legislative Budget Board, 2025, p. 30

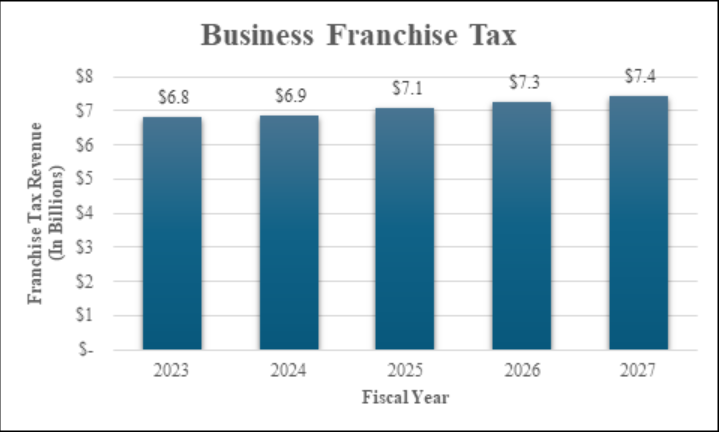

Over a five-year time horizon, franchise tax revenue growth has been relatively stagnant. In FY 2023, the tax generated approximately $6.8 billion (see Figure 2). By FY 2027, tax collections are projected to increase to $7.4 billion, which is a 9.2% growth rate. For the period, the year-over-year growth rates are as follows: 0.6%; 3.2%; 2.8%; and 2.3%, respectively (Legislative Budget Board, 2025, p. 30).

Figure 2

Franchise Tax Revenue Growth, FYs 2023 – 2027

Source: Legislative Budget Board, 2025, p. 30

An Opportunity for Reform

There is ample evidence to suggest that Texas’s business franchise tax is less than ideal and in need of reform. It is complex for taxable entities to comply with; it still applies to too many small and medium-sized businesses (i.e., those with taxable margins in excess of $2.65 million)1; and it generates a relatively modest amount of tax revenue in the context of the state’s larger fiscal picture. In light of these concerns, it would be prudent for the next Texas Legislature to consider eliminating the franchise tax—and there are many sound economic reasons to do so.

Studies modeling the dynamic effects of phasing out or repealing the franchise tax provide compelling economic justifications for considering such an approach, including the creation of thousands of net new private sector jobs and generating billions in net new personal income. In 2015, Texas Public Policy Foundation (TPPF) scholars created a dynamic economic model that established the private sector’s burdens and compliance costs in relation to the tax. These scholars used a 3- variable recursive vector autoregressive (VAR) model to estimate the tax’s impact on income and employment. The three variables measured were the percent changes in real personal income (PI), total private-sector nonfarm employment, and real margin tax revenue (Ginn & Heflin, 2015). The study found that, beginning in 2008 when the tax was implemented, real income and private-sector employment were adversely impacted. In fact, when franchise tax revenue was at its peak, personal income and employment were significantly depressed (Ginn & Heflin, 2015). This conforms to the idea that taxes on capital have a negative effect on investment. Higher costs of doing business can prevent business expansion, which ultimately slows employment and wage growth (Ginn & Heflin, 2015). Based on TPPF’s model, it is estimated that a complete elimination of the franchise tax could create at least $16 billion in new inflation-adjusted total personal income and more than 130,000 new jobs over a five-year time horizon (Ginn & Heflin, 2015).

By moving in this direction, policymakers could further solidify Texas’ economic dominance and incentivize additional job creation, business investment, and income growth. Moreover, the initiative would alleviate the burden on existing businesses, potentially benefiting a wide array of Texans. Let us remember that businesses do not pay taxes; people do. Thus, when business owners bear higher taxes, those costs tend to be passed along to various parties in the form of higher prices, lower wages, fewer job opportunities, lower returns on investment, or upstream effects on suppliers.

In light of these concerns, it would serve Texas well for policymakers to eliminate the franchise tax. Its negative effects are felt by almost everyone, including consumers, employees, job seekers, shareholders, and suppliers. And the weight of its burden is very much disproportionate to the benefit it confers on the state’s revenues.

Fast Facts

- For FYs 2026 and 2027, the franchise tax is expected to generate $7.3 billion and $7.4 billion, respectively.

- Franchise tax collections are expected to represent 8.4% of all tax revenue and 4.1% of total revenues.

- Economic models suggest that eliminating the franchise tax could result in robust private sector job creation and personal income growth.

References

Ginn, V., & Heflin, T. (2015). Economic effects of eliminating Texas’ business margin tax. Texas Public Policy Foundation. https://www.texaspolicy.com/wp-content/uploads/2018/08/MarginTax-CFP.pdf

Legislative Budget Board. (2020). Study on district property tax compression. https://www.lbb.texas.gov/Documents/Publications/Policy_Report/6391_HB3_Revenue_Policy_Report.pdf

Legislative Budget Board. (2025). Fiscal size-up: 2026-27 biennium. https://www.lbb.texas.gov/documents/publications/fiscal_sizeup/fiscal_sizeup.pdf

SB 3 Bill Analysis. Senate Research Center. 88th Legislative Session. 2nd Called Session. (2023, July). https://capitol.texas.gov/tlodocs/882/analysis/pdf/SB00003F.pdf

Texas Comptroller of Public Accounts. (n.d.-a). Franchise tax. Retrieved June 1, 2026, from https://comptroller.texas.gov/taxes/franchise/index.php#what-is-ft

Texas Comptroller of Public Accounts. (n.d.-b). Franchise tax overview. Retrieved June 1, 2026, from https://comptroller.texas.gov/taxes/publications/98-806.php

Texas Comptroller of Public Accounts. (n.d.-c). No tax due reporting for report years 2024 and later. Retrieved June 1, 2026, from https://comptroller.texas.gov/taxes/franchise/ntd-rpt-updates-2024.php

Texas Comptroller of Public Accounts. (2025, December). Taxes of Texas: A field guide. Retrieved June 1, 2026, from https://comptroller.texas.gov/transparency/revenue/docs/96-1774.pdf