The Biden administration has released its plans to introduce a new income-driven repayment program for student loans. The proposed regulations are as bad as the early indications hinted they would be.

For those just getting up to speed, a standard loan uses a fixed monthly payment and a predetermined number of payments (e.g., a car loan of $500 per month for five years). If you borrow more, your monthly payment goes up. In contrast, income-driven loans base your payment on your current income, while the number of payments varies (e.g., 10% of income until you’ve repaid the loan). If you borrow more in an income-driven loan, your monthly payment is completely unaffected, but you will repay for longer.

For student lending, income-driven loans have two huge advantages over standard loans. First, you have to go out of your way to default on an income-driven loan (if your income drops to $0, so does your monthly payment), so income-driven lending will effectively eliminate student loan defaults. Second, income-driven loans naturally smooth consumption over time. While a fixed-payment loan will impose a high financial burden when your income is low and a small burden when your income is high, an income-driven loan will impose a higher burden as income increases.

Unfortunately, income-driven repayment is being hijacked by progressives to provide massive new subsidies to colleges and universities.

For starters, a cap on the length of repayment required (i.e., after the cap is reached, any remaining balance is forgiven) breaks the moderating mechanism of income-driven repayment. A cap is fundamentally unnecessary in an income-driven repayment plan because, by definition, payments are always affordable.

Unfortunately, politicians have found lowering the cap irresistible. While the first income-driven repayment program had a cap of 25 years, and most others had a cap of 20 years, Biden is lowering it to 10 years for some borrowers. But altering the length of repayment is precisely how income-driven loans account for loans of different size (since payments are based on income, not loan size). Capping the length of repayment is equivalent to capping monthly payments in a standard loan, regardless of how much is borrowed. Such a foolish policy would break borrower discipline for standard loans, leading to massive overborrowing. The same principle and outcome applies to the income-driven loans, though in this case, the cap is the number of payments.

But the bigger problem is that progressives are ditching the “income” and “repayment” parts of income-driven repayment. They do this by exempting a large share of income from any repayment, while simultaneously lowering the share of non-exempted income owed.

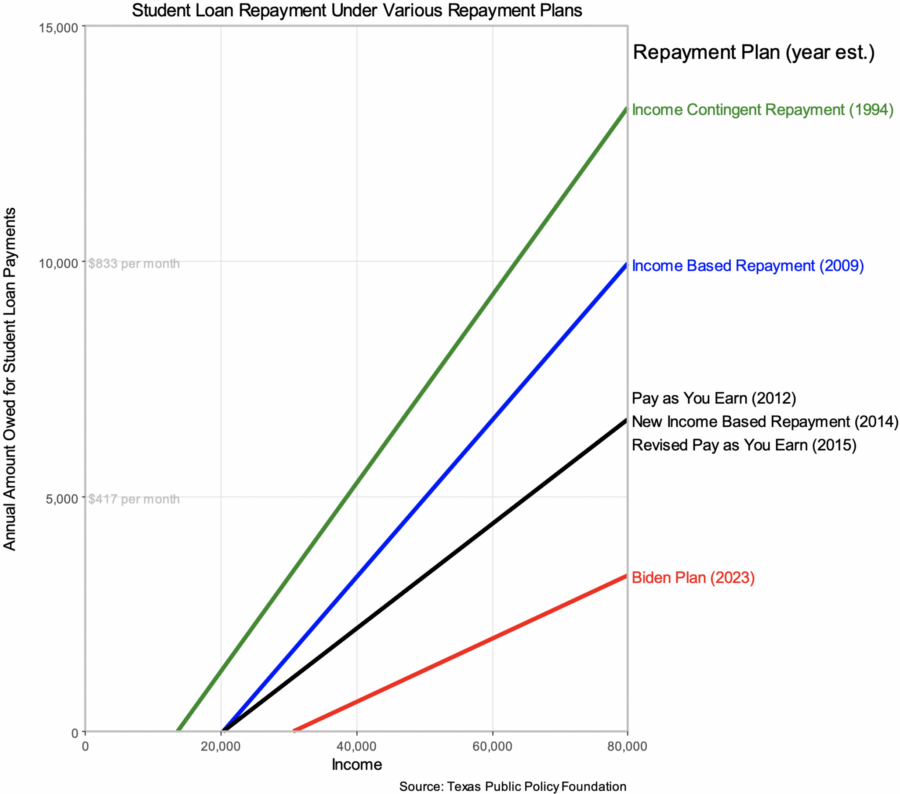

The first income-driven repayment program (established in 1994) set payments at 20% of income above the poverty line. Later income-driven programs set payments at 10–20% of income above 150% of the poverty line. Biden is setting payments at just 5% of income above 225% of the poverty line. These changes have a multiplier effect in lowering student loan repayments, as can be seen in the figure below (slightly modified from our earlier investigation), which shows student loan payments by income under the historical and proposed income-driven repayment plans.

The Biden plan’s extremely generous income exemptions and repayment-rate reductions transform student loan payments from a method of repaying loans into merely symbolic payments.

Consider associate degree graduates. The median earnings of associate degree graduates three years after graduation is $34,000. Yet over $30,000 is exempted from repayment, yielding a monthly loan payment of just $15 a month. The median borrower took out $14,000, so the median student’s annual payments ($180) wouldn’t even pay the interest on the loan ($700, at the current 5% interest rate). This student will repay none of what he borrowed, and since Biden is also going to waive any unpaid interest, he will even have 75% of the interest forgiven.

Nor will the median bachelor’s degree graduate repay any of his loans. Recent bachelor’s degree graduates earn a median of $47,000, and among borrowers, the median amount borrowed was $24,000. The median student would have a monthly payment of $68, and his annual payments ($816) wouldn’t even cover the interest on his loan ($1,200). Thus, the median bachelor’s degree graduate will repay none of what he borrowed and will have about one-third of the interest waived as well.

When the median associate’s or bachelor’s degree graduate will not repay a single penny of his loan, we are no longer talking about a loan repayment program. Instead, the Biden administration has converted student loans into a delayed grant program.