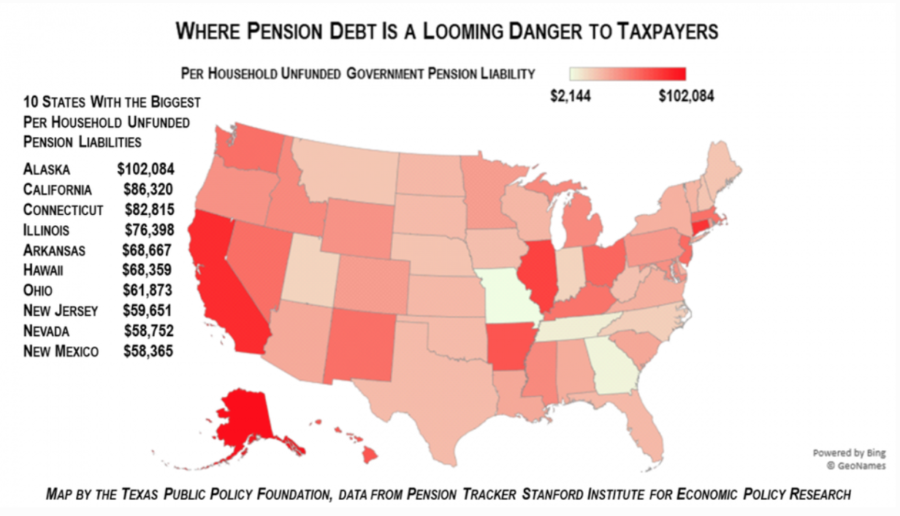

Pension Tracker, a project of the Stanford Institute for Economic Policy Research led by former California State Assemblyman Joe Nation, Ph.D., is out with its updated assessment of the nation’s unfunded state and local government pension fund liabilities. It’s not a pretty picture—especially if you live in Alaska, California, Connecticut or Illinois where your per household pension debt ranges from $102,084 to $76,398.

While the healthy economy and rising stock market has lifted pension fund investments around the nation, most pension funds assume unrealistically high returns and expose taxpayers to significant risk if their investment decisions don’t return projected earnings.

State and local governments, including public schools, either pay into Social Security just as private sector employers do, or they run their own pension systems.

As with anything government does, there are increasingly large stakes in the outcome as government gets bigger and more powerful. This is no different with pensions for government employees, where powerful government employee labor unions, controlling more than a billion dollars of annual spending at the federal and state level, lobby elected officials to increase the value of their members’ pensions.

A pension is a form of deferred compensation. An employee and employer agree to set aside a portion of the employee’s salary payable upon retirement. Originally, government pensions were designed as an incentive to encourage nonproductive bureaucrats to leave service earlier than they might otherwise do to thin out the dead wood in an organization. Over time, pensions became more generous and the time of service required to retire reduced.

Government pension systems are generally funded by four revenue sources that vary in each jurisdiction: deductions from an employee’s paycheck; contributions from the employer; investment earnings from the pension fund; and taxpayers.

As new employees come into the system, their deductions and employer contributions are paying for the retirees who are no longer working.

In theory, the system is supposed to be self-sustaining. Paycheck deductions, employer contributions and investment income are supposed to meet retiree obligations over an amortized period, often 20 years. Shortfalls—unfunded liabilities—are supposed to be made up by increasing paycheck deductions and employer contributions as increasing investment income is coupled with increased risk which in turn puts taxpayers at greater risk of a pension fund bailout.

But politics happens. In good times, pension fund investment income from Wall Street and other investment pours in, making the pension fund look fiscally sound. Politicians are reluctant to salt away added funds when the pension balance sheet looks strong. But in bad times, when investment returns go negative, government income also tends to be weak, leaving legislators with little appetite to put more money in to the pension fund. What often ended up happening is that the pension fund would be tacitly encouraged to report unrealistically high earnings expectations over their 20-year amortization, thus presenting to lawmakers and the public the appearance of a fiscally sound pension fund. This sound appearance was a mirage.

The most notable example of this occurred in 1999. Senate Bill 400 passed that year in California. SB 400 granted tens of billions of dollars in retroactive increases to pension benefits on the assurance from the nation’s largest government pension system, the California Public Employees’ Retirement System (CalPERS), along with the state’s powerful government labor unions, that the state’s main pension plans were overfunded by as much as $17.6 billion.

The fund was in good shape at the time, as it was heavily invested in the Dot.com boom on Wall Street. The boom went bust soon after the higher benefits were granted with the 9-11 attacks following on soon after. In less than two years, California’s massive pension system was seriously in the red.

This matters for taxpayers in California—and other states—because pension obligations, once made, are virtually impossible to renegotiate or discharge. Since states are sovereign entities with unlimited ability to tax, and because they cannot declare bankruptcy, any government pension shortfall must eventually be paid by the taxpayer.

In California, state and local governments have started feeling the practical pinch of these past pension promises, with taxpayer support of the state pensions for teachers and other government employees rising from $611 million in 2001 to $3.5 billion in 2010. Local governments were hit hard for past promises to government workers. San Jose’s pension expenses ballooned from $73 million in 2001 to $245 million in 2010. As a result, government services were often trimmed to make good on guaranteed pension payments.

Former California Gov. Jerry Brown supported legislation to reduce pension benefits for new employees, increasing the retirement age and increasing employee payroll deductions and employer contributions. Even so, California school districts are expected to pay $5.7 billion towards the pension obligations for retired teachers this year.

Pension Tracker has collected data from around the nation, and in California specifically, has gathered information from more than 1,200 counties, cities, and special districts to determine that the total market pension debt in California is more than $1 trillion, or $78,334 per household, the second-highest in the nation after Alaska. Nationally, Pension Tracker calculates the total pension debt on a market basis at $5.2 trillion, or an average of $43,179 per household.

Unless pension funds around the nation continue to earn 7% or more per year on their investments, it’s likely that taxpayers will be on the hook for trillions of dollars of promises to government unions. These promises have been made by politicians past and present, resulting in pressure to increase taxes and cut government services.